Pricing Asian option under mixed jump-fraction process

|

|

|

- Ελλεν Ασπάσιος

- 7 χρόνια πριν

- Προβολές:

Transcript

1 3 17 ( ) Journal of Eas China Normal Universiy (Naural Science) No. 3 May 17 : 1-641(17) ( 18) : -. Iô.... : -; ; : O11.6 : A DOI: /j.issn Pricing Asian opion under mixed jump-fracion process GENG Yan-jing ZHOU Sheng-wu (Deparmen of Mahemaics China Universiy of Mining and Technology Xuzhou Jiangsu 18 China) Absrac: This paper mainly sudied he geomeric average Asian opion pricing on he condiion ha he underlying asse followed mixed jump-fracion process. The general Iô s lemma and he self-financing dynamic sraegy were obained by using he parial differenial equaion of such opion pricing in he mixed fracional environmen wih jump. Wih he combinaion of boundary condiion an analyic formula for he geomeric average Asian opion was derived by solving he parial differenial equaion. The numerical experimens were showed o discuss he influence of differen parameers on he opion value. The resuls were he generalizaion of some exising resuls which was closer o he real financial marke. Key words: mixed jump-fracion process; geomeric average Asian opion; parial differenial equaion. Kemna Vors [1 : : (13XK3) :. gengyanjing ah@qq.com. :. zswcum@163.com.

2 3 ( ) 17 ; Wong Cheung [ ; Ching-Sung Chou [3 -. ( ) ;. Markov Iô. Cheridio [4-. Kuznesov [6 Zähle [7 Mishura [8 Black-Scholes. [9-1 Black-Scholes. Poisson. Farshid Mehrdous [11 ; Nisha Rambeerich [1 -.. [13 - ; [14 - Iô. [1 [16 - Iô. FoadShokrollahi [ Black-Scholes. 1. ds = (µ q )S d + σs (dm + dn ) (1) µ q σ M H = B + B H B B H H ( 1) ; N = Q λ Q λ Q B B H. 1( - Iô ) W = B + B H + N f( x) C 1 (R + R R) f( W ) τ (τ W τ)dτ f x (τ W τ )dτ f x (τ W τ )τ H 1 dτ L (P)

3 3 : - 31 f( W ) =f( ) + x (τ W τ)dw τ + [ τ (τ W τ) + 1 (1 + λ + HτH 1 ) f x (τ W τ) dτ. () N i i. W = B + B H + Q λ i = 1 W ( ) 1 ( 1 ) ( 1 ) Iô f( 1 W ) = f( ) [ τ + 1 (1 + HτH 1 ) f 1 x λ dτ + x x db τ + [ f( W ) = f( 1 W 1 ) + 1 τ + 1 (1 + HτH 1 ) f x λ dτ + x f( W ) 1 f( 1 W 1 ) f( 1 W ) 1 [ f( W ) =f( ) + τ + 1 (1 + HτH 1 ) f i ( ) f( W ) =f( ) + x λ x 1 x db τ + dτ + x db τ + x dbh τ + f( 1 W 1 ) f( 1 W ). 1 [ τ + 1 (1 + HτH 1 ) f x λ dτ x + x db τ + x dbh τ + f(τ W τ ) f(τ W τ ). τ g(φ) C (R R) (dq dq ) = λd g(q ) Iô [14 τ [ g(q τ ) g(q τ ) = g (Q τ )dq τ + λ g (Q τ )dτ. 1 x dbh τ 1 x dbh τ. W = B + B H + Q λ τ [ f(τ W τ ) f(τ W τ ) = x dq τ + λ f x dτ. f( W ) =f( ) + + x db τ + =f( ) + [ τ + 1 (1 + HτH 1 ) f x λ x dτ x dbh τ + x dq τ + λ f x dτ [ τ + 1 (1 + λ + HτH 1 ) f x λ dτ + x x dw τ.

4 3 ( ) 17 (1) { S = S exp (µ τ q τ )dτ σ (H + λ + ) + σw }. (3) f( W ) = S exp { (µ τ q τ )dτ σ (H + λ + ) + σw } 1. 3 S - (1) K T ( T) V c ( J S ) : + (r q )S + 1 S σ S V S + J (lns lnj ) J = r V (4) T < S < + < J < + σ = σ (1 + H H 1 + λ) V c (T J T S T ) = (J T K) +. V = V c ( J S ) J J = e 1 [ ( dj = J 1 lns τ dτ + 1 ) lns lns lnj = J. ln Sτdτ : dp = r P d ds = (µ q )S d + σs (db + db H + dn ) θ = (θ θ 1 ) V = θ P + θ 1 S 1 dv = θ dp + θ 1 ds + θ 1 q S d dv = θ dp + θ 1 ds + θ 1 q S d = (V θ 1 S )r d + θ 1 (µ q )S d + θ 1 σs dw + θ 1 q S d = (V θ 1 S )r d + θ 1 µ S d + θ 1 σs dw. [ dv = + (µ q )S + lns lnj S J J d + 1 σ S (1 + H H 1 + λ) V S d + σs dw. S

5 3 : - 33 θ 1 = S µ S S d + r V d r S S d + σs S dw = d + [(µ q )S d + σs dw S + dj + 1 J V S [σ S (d + HH 1 d + λd) r V = + (r ln S ln J q )S S + J J + 1 σ S (1 + HH 1 + λ) V. σ = S σ (1 + H H 1 + λ). r V = + (r q )S + lns lnj S J + 1 J σ S V S. 4 S - (1) K T ( T) V c ( J S ) T V c ( J S ) =(J ST ) 1 T exp {r (T ) T r (r θ q θ ) T θ = T dθ T σ H = r θ dθ + (σ H ) (T H H ) + (σ λ ) (T ) }N(d 1 ) Ke T rθdθ N(d ) () (λσ + σ )(T ) 4T σ (T H H ) (T ) + Hσ (T H+1 H+1 ) (H + 1)(T ) [ 1 4H(T H+1 H+1 ) (H + 1)(T H H ) + H(T H+ H+ ) 1 σ T (H + 1)(T H H σλ = T ( λ + 1σ) ) 3T (σλ ) (T ) + (σh ) (T H H ) + 1 d 1 = T ln J S T K T + r (T ) (σ λ ) (T ) + (σh ) (T H H ) d = d 1 (σλ ) (T ) + (σh ) (T H H ) N(x) = 1 x e d. π 3 ( T) V c ( J S ) (4). ξ = 1 T [ lnj + (T )lns V c ( J S ) = U( ξ )

6 34 ( ) 17 = U + U lnj lns ξ T = U T = U S ξ TS J ξ TJ V S = ( U T ) ( T ) U = S ξ TS TS ξ T TS U ξ (4) U ( + r q 1 ) T σ U + 1 ( T ) U T ξ σ T ξ U(T ξ T ) = (e ξt K) +. = r U (6) α() β() γ() τ = γ() η τ = ξ + α() W(τ η τ ) = U( ξ )e β() U = e β()[ W τ γ () β ()W + W α () η τ U ξ = e β() W η τ U ξ = ( e β() W ) = e β() W ξ η τ ητ (6) γ () W [ τ + α () + (r q 1 σ ) T W T η τ + 1 σ( T ) W T ητ (r + β ())W =. (7) γ () + 1 σ( T ) ( = α () + r q 1 T σ) T = r + β () = T α(t) = β(t) = γ(t) = β() = α() = T T r θ dθ γ() = σ + λσ 6 (r θ q θ )dθ σ + λσ (T )3 T 4T (T ) + Hσ (T H+1 H+1 ) T(H + 1) [ + Hσ T H H + (T H+ H+ ) H T (H + 1) σ (T H H ) 4(T H+1 H+1 ) T(H + 1)

7 3 : - 3 (7) W τ = W ητ W( η ) = (e η K) + (8) (8) W(τ η τ ) = 1 πτ = 1 πτ = I 1 + I. + + (e y K)e (y η τ ) 4τ dy e y e (y η τ ) 4τ dy K πτ + e (y η τ ) 4τ dy I 1 = 1 πτ = e τ+η τ π y η τ τ τ = e y e (y η τ ) 4τ dy = e τ+η τ η τ +τ τ 1 + π e (y η τ τ) 4τ dy e d = e τ+η τ N ( ητ + τ lnk τ ). I = K πτ + y η τ τ = e (y η τ ) 4τ dy = K + π η τ π e ( ητ lnk d = KN ). π (8) ( W(τ η τ ) = e τ+η ητ + τ lnk ) ( ητ lnk ) τ N KN τ τ d 1 = τ + η τ lnk τ = d = η τ lnk τ = = e τ+η τ N(d1 ) KN(d ). (9) (σλ ) (T ) + (σh ) (T H H ) + 1 T ln J ST (σ λ ) (T ) + (σh ) (T H H ) 1 T ln J S T K T + r (T ) (σ λ ) (T ) + (σh ) (T H H ) = d 1 (σλ ) (T ) + (σh ) (T H H ). K T + r (T )

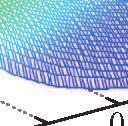

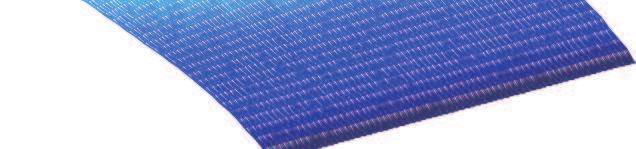

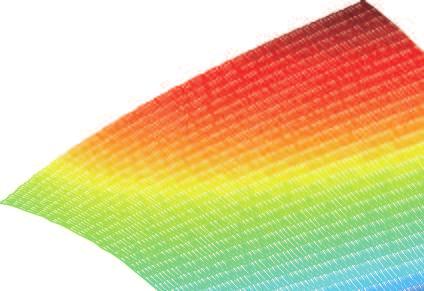

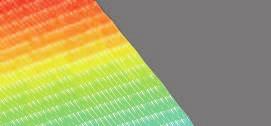

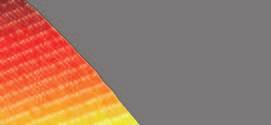

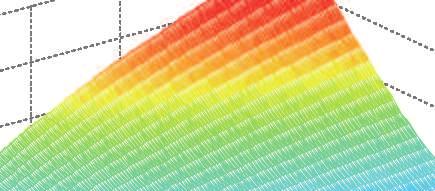

8 36 ( ) 17 1 S - (1) K T ( T) V p ( J S ) T V p ( J S ) = (J ST ) 1 T exp {r (T ) 4. r θ dθ + (σ H ) (T H H ) + (σ λ ) (T ) }N( d 1 ) + Ke T rθdθ N( d ). (1) V (T J T S T ) = (K J T ) + 3 (4) V p ( J S ) (1). S = 8 K = 8 σ =.4 r =. q =.1 S = 8 = T = 1 r =. q =.1 σ =.4 K = /V H =.1 H =.3 H =. H =.7 H = /S /V P H H =.1 H =.3 H =. H =.7 H = /S Fig. 1 Asian opion pricing corresponding o differen H

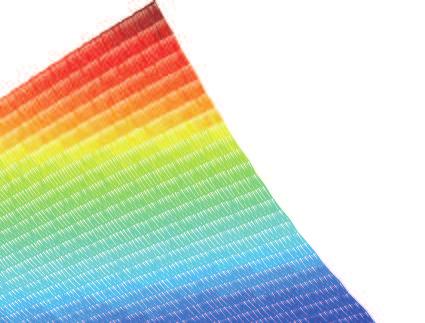

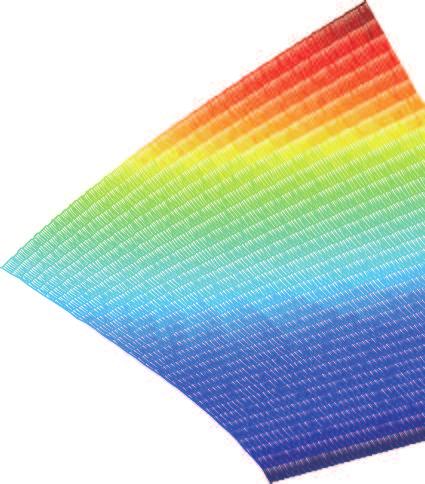

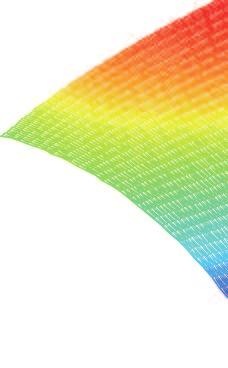

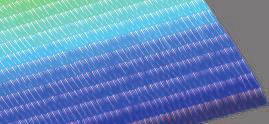

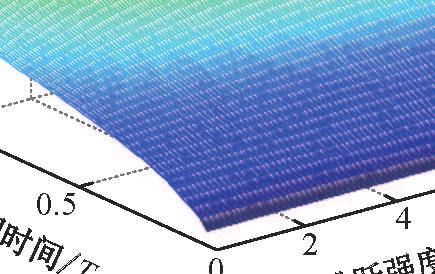

9 13Ï ñò : Ü êa-*ñ.e æªï ½d 4 6 lambda = lambda = lambda = 4 lambda = 6 ⴻ ᵏᵳԧ /V 3 lambda = lambda = lambda = 4 lambda = 6 ⴻ䏼ᵏᵳԧ /V 㛑 ԧṭ /S 4 6 Fig. Asian opion pricing corresponding o differen λ ⴻ䏼ᵏᵳԧ /Vp 1 ⴻ ᵏᵳԧ /Vc ᵏ. 䰤 T. ã3 Fig H. ᮠ 䎛ᯟ ᵏ. 䰤 T ᮠ H 䎛ᯟ 1. âda ê! Ï múæªï d 'X The relaion of Hurs exponen expiry dae and Asian opion ⴻ䏼ᵏᵳԧ /Vp 㛑 ԧṭ /S éaøó λ æªï d ã ⴻ ᵏᵳԧ /Vc T ã4 Fig. 4 4 ( bda Lam ᕪᓖ 䐣䏳 6 T bda Lam ᕪᓖ 䐣䏳 a rý! Ï múæªwþï d 'X The relaion of jump inensiy expiry dae and Asian opion Ø b d v Ü êa-*ñl ÏL Iˆo ÚnÚgK üñí Ñ Ü êùk$äe a æªï ½d. $^CþO {é½d.?1 )

10 38 ( ) 17.. [ [ 1 KEMNA A G Z VORST A C F. A pricing mehod for opions based on average asse values [J. Journal of Banking and Finance (1): [ WONG H Y CHEUNG H L. Geomeric Asian opions: Valuaion and calibraion wih sochasic volailiy [J. Quaniaive Finance 4 4(3): [ 3 CHOU C S LIN H J. Asian opions wih jumps [J. Saisics & Probabiliy 6 6(14): [ 4 CHERIDITO P. Regularizing fracional Brownian moion wih a view owards sock price modelling [D. Zürich: Swiss Federal Insiue of Technology 1. [ CHERIDITO P. Arbirage in fracional Brownian moion models [J. Finance and Sochasics 3 7(4): [ 6 KUZNETSOV Y A. The absence of arbirage in a model wih fracal Brownian moion [J. Russian Mahemaical Surveys (4): [ 7 ZÄHLE M. Long range dependence no arbirage and he Black Scholes formula [J. Sochasics and Dynamics (): 6-8. [ 8 MISHURA Y S. Sochasic Calculus for Fracional Brownian Moion and Relaed Processes [M. Berlin: Springer 8. [ 9 WANG X T. Scaling and long-range dependence in opion pricing I: Pricing European opion wih ransacion coss under he fracional Black Scholes model [J. Physica A 1 389(3): [1 WANG X T. Scaling and long-range dependence in opion pricing V: Muliscaling hedging and implied volailiy smiles under he fracional Black Scholes model wih ransacion coss [J. Physica A 11 39(9): [11 MEHRDOUST F SABER N. Pricing arihmeic Asian opion under a wo-facor sochasic volailiy model wih jumps [J. Journal of Saisical Compuaion and Simulaion 1 8(18): [1 RAMBEERICH N. A high order finie elemen scheme for pricing opions under regime swiching jump diffusion processes [J. Journal of Compuaional and Applied Mahemaics 16 3(): [13 XIAO W L. Pricing currency opions in a fracional Brownian moion wih jumps[j. Economic Modelling 1 7(): [14 PENG B. Pricing Asian power opions under jump-fracion process [J. Journal of Economics Finance and Adminisraive Science 1 17(33): -9. [1. [J. ( ) 13 3(6): 9-9. [16. [J. 13 3(11): [17 SHOKROLLAHI F. Acuarial approach in a mixed fracional Brownian moion wih jumps environmen for pricing currency opion [J. Advances in Difference Equaions 1 7(1): 1-8. (: )

Vulnerable European option pricing with the time-dependent for double jump-diffusion process

1 014 1 Journal of Eas China Normal Universiy Naural Science No. 1 Jan. 014 : 1000-564101401-0013-08 -,, 1116 :,., r σ d ;, Iô,. : ; ; : O11.6 : A DOI: 10.3969/j.issn.1000-5641.014.01.003 Vulnerable European

1 014 1 Journal of Eas China Normal Universiy Naural Science No. 1 Jan. 014 : 1000-564101401-0013-08 -,, 1116 :,., r σ d ;, Iô,. : ; ; : O11.6 : A DOI: 10.3969/j.issn.1000-5641.014.01.003 Vulnerable European

: Ω F F 0 t T P F 0 t T F 0 P Q. Merton 1974 XT T X T XT. T t. V t t X d T = XT [V t/t ]. τ 0 < τ < X d T = XT I {V τ T } δt XT I {V τ<t } I A

![: Ω F F 0 t T P F 0 t T F 0 P Q. Merton 1974 XT T X T XT. T t. V t t X d T = XT [V t/t ]. τ 0 < τ < X d T = XT I {V τ T } δt XT I {V τ<t } I A](/thumbs/91/105433318.jpg ": Ω F F 0 t T P F 0 t T F 0 P Q. Merton 1974 XT T X T XT. T t. V t t X d T = XT [V t/t ]. τ 0 < τ < X d T = XT I {V τ T } δt XT I {V τ<t } I A") 2012 4 Chinese Journal of Applied Probability and Statistics Vol.28 No.2 Apr. 2012 730000. :. : O211.9. 1..... Johnson Stulz [3] 1987. Merton 1974 Johnson Stulz 1987. Hull White 1995 Klein 1996 2008 Klein

2012 4 Chinese Journal of Applied Probability and Statistics Vol.28 No.2 Apr. 2012 730000. :. : O211.9. 1..... Johnson Stulz [3] 1987. Merton 1974 Johnson Stulz 1987. Hull White 1995 Klein 1996 2008 Klein

Vol. 40 No Journal of Jiangxi Normal University Natural Science Jul. 2016

4 4 Vol 4 No 4 26 7 Journal of Jiangxi Normal Universiy Naural Science Jul 26-5862 26 4-349-5 3 2 6 2 67 3 3 O 77 9 A DOI 6357 /j cnki issn-5862 26 4 4 C q x' x /q G s = { α 2 - s -9 2 β 2 2 s α 2 - s

4 4 Vol 4 No 4 26 7 Journal of Jiangxi Normal Universiy Naural Science Jul 26-5862 26 4-349-5 3 2 6 2 67 3 3 O 77 9 A DOI 6357 /j cnki issn-5862 26 4 4 C q x' x /q G s = { α 2 - s -9 2 β 2 2 s α 2 - s

J. of Math. (PRC) u(t k ) = I k (u(t k )), k = 1, 2,, (1.6) , [3, 4] (1.1), (1.2), (1.3), [6 8]

![J. of Math. (PRC) u(t k ) = I k (u(t k )), k = 1, 2,, (1.6) , [3, 4] (1.1), (1.2), (1.3), [6 8]](/thumbs/91/107007576.jpg "J. of Math. (PRC) u(t k ) = I k (u(t k )), k = 1, 2,, (1.6) , [3, 4] (1.1), (1.2), (1.3), [6 8]") Vol 36 ( 216 ) No 3 J of Mah (PR) 1, 2, 3 (1, 4335) (2, 4365) (3, 431) :,,,, : ; ; ; MR(21) : 35A1; 35A2 : O17529 : A : 255-7797(216)3-591-7 1 d d [x() g(, x )] = f(, x ),, (11) x = ϕ(), [ r, ], (12) x(

Vol 36 ( 216 ) No 3 J of Mah (PR) 1, 2, 3 (1, 4335) (2, 4365) (3, 431) :,,,, : ; ; ; MR(21) : 35A1; 35A2 : O17529 : A : 255-7797(216)3-591-7 1 d d [x() g(, x )] = f(, x ),, (11) x = ϕ(), [ r, ], (12) x(

High order interpolation function for surface contact problem

3 016 5 Journal of East China Normal University Natural Science No 3 May 016 : 1000-564101603-0009-1 1 1 1 00444; E- 00030 : Lagrange Lobatto Matlab : ; Lagrange; : O41 : A DOI: 103969/jissn1000-56410160300

3 016 5 Journal of East China Normal University Natural Science No 3 May 016 : 1000-564101603-0009-1 1 1 1 00444; E- 00030 : Lagrange Lobatto Matlab : ; Lagrange; : O41 : A DOI: 103969/jissn1000-56410160300

DOI /J. 1SSN

4 3 2 Vol 43 No 2 2 1 4 4 Journal of Shanghai Normal UniversityNatural Sciences Apr 2 1 4 DOI1 3969 /J 1SSN 1-5137 214 2 2 1 2 2 1 22342 2234 O 175 2 A 1-51372142-117-1 2 7 8 1 2 3 Black-Scholes-Merton

4 3 2 Vol 43 No 2 2 1 4 4 Journal of Shanghai Normal UniversityNatural Sciences Apr 2 1 4 DOI1 3969 /J 1SSN 1-5137 214 2 2 1 2 2 1 22342 2234 O 175 2 A 1-51372142-117-1 2 7 8 1 2 3 Black-Scholes-Merton

Levin Lin(1992) Oh(1996),Wu(1996) Papell(1997) Im, Pesaran Shin(1996) Canzoneri, Cumby Diba(1999) Lee, Pesaran Smith(1997) FGLS SUR

Oh(1996),Wu(1996) Papell(1997) Im, Pesaran Shin(1996) Canzoneri, Cumby Diba(1999) Lee, Pesaran Smith(1997) FGLS SUR") EVA M, SWEEEY R 3,. ;. McDonough ; 3., 3006 ; ; F4.0 A Levin Lin(99) Im, Pesaran Shin(996) Levin Lin(99) Oh(996),Wu(996) Paell(997) Im, Pesaran Shin(996) Canzoner Cumby Diba(999) Levin Lin(99) Coe Helman(995)

EVA M, SWEEEY R 3,. ;. McDonough ; 3., 3006 ; ; F4.0 A Levin Lin(99) Im, Pesaran Shin(996) Levin Lin(99) Oh(996),Wu(996) Paell(997) Im, Pesaran Shin(996) Canzoner Cumby Diba(999) Levin Lin(99) Coe Helman(995)

Credit Risk. Finance and Insurance - Stochastic Analysis and Practical Methods Spring School Jena, March 2009

Credit Risk. Finance and Insurance - Stochastic Analysis and Practical Methods Spring School Jena, March 2009 1 IV. Hedging of credit derivatives 1. Two default free assets, one defaultable asset 1.1 Two

Credit Risk. Finance and Insurance - Stochastic Analysis and Practical Methods Spring School Jena, March 2009 1 IV. Hedging of credit derivatives 1. Two default free assets, one defaultable asset 1.1 Two

& Risk Management , A.T.E.I.

Μεταβλητότητα & Risk Managemen Οικονοµικό Επιµελητήριο της Ελλάδας Επιµορφωτικά Σεµινάρια Σταύρος. Ντεγιαννάκης, Οικονοµικό Πανεπιστήµιο Αθηνών Χρήστος Φλώρος, A.T.E.I. Κρήτης Volailiy - Μεταβλητότητα

Μεταβλητότητα & Risk Managemen Οικονοµικό Επιµελητήριο της Ελλάδας Επιµορφωτικά Σεµινάρια Σταύρος. Ντεγιαννάκης, Οικονοµικό Πανεπιστήµιο Αθηνών Χρήστος Φλώρος, A.T.E.I. Κρήτης Volailiy - Μεταβλητότητα

d dt S = (t)si d dt R = (t)i d dt I = (t)si (t)i

si d dt R = (t)i d dt I = (t)si (t)i") d d S = ()SI d d I = ()SI ()I d d R = ()I d d S = ()SI μs + fi + hr d d I = + ()SI (μ + + f + ())I d d R = ()I (μ + h)r d d P(S,I,) = ()(S +1)(I 1)P(S +1, I 1, ) +()(I +1)P(S,I +1, ) (()SI + ()I)P(S,I,)

d d S = ()SI d d I = ()SI ()I d d R = ()I d d S = ()SI μs + fi + hr d d I = + ()SI (μ + + f + ())I d d R = ()I (μ + h)r d d P(S,I,) = ()(S +1)(I 1)P(S +1, I 1, ) +()(I +1)P(S,I +1, ) (()SI + ()I)P(S,I,)

The martingale pricing method for pricing fluctuation concerning stock models of callable bonds with random parameters

32 Vol 32 2 Journal of Harbin Engineering Univerity Jan 2 doi 3969 /j in 6-743 2 23 5 2 F83 9 A 6-743 2-24-5 he martingale pricing method for pricing fluctuation concerning tock model of callable bond

32 Vol 32 2 Journal of Harbin Engineering Univerity Jan 2 doi 3969 /j in 6-743 2 23 5 2 F83 9 A 6-743 2-24-5 he martingale pricing method for pricing fluctuation concerning tock model of callable bond

A Control Method of Errors in Long-Term Integration

1,a) Hamilon Runge Kua Hamilonian 1/2 Runge Kua (Brouwer s law) Runge Kua Runge Kua Hamilonian 1/2 Brouwer 3 A Conrol Mehod of Errors in Long-Term Inegraion Ozawa Kazufumi 1,a) Absrac: When solving he

1,a) Hamilon Runge Kua Hamilonian 1/2 Runge Kua (Brouwer s law) Runge Kua Runge Kua Hamilonian 1/2 Brouwer 3 A Conrol Mehod of Errors in Long-Term Inegraion Ozawa Kazufumi 1,a) Absrac: When solving he

ACTA MATHEMATICAE APPLICATAE SINICA Nov., ( µ ) ( (

( (") 35 Þ 6 Ð Å Vol. 35 No. 6 2012 11 ACTA MATHEMATICAE APPLICATAE SINICA Nov., 2012 È ÄÎ Ç ÓÑ ( µ 266590) (E-mail: jgzhu980@yahoo.com.cn) Ð ( Æ (Í ), µ 266555) (E-mail: bbhao981@yahoo.com.cn) Þ» ½ α- Ð Æ Ä

35 Þ 6 Ð Å Vol. 35 No. 6 2012 11 ACTA MATHEMATICAE APPLICATAE SINICA Nov., 2012 È ÄÎ Ç ÓÑ ( µ 266590) (E-mail: jgzhu980@yahoo.com.cn) Ð ( Æ (Í ), µ 266555) (E-mail: bbhao981@yahoo.com.cn) Þ» ½ α- Ð Æ Ä

( ) ( t) ( 0) ( ) dw w. = = β. Then the solution of (1.1) is easily found to. wt = t+ t. We generalize this to the following nonlinear differential

( t) ( 0) ( ) dw w. = = β. Then the solution of (1.1) is easily found to. wt = t+ t. We generalize this to the following nonlinear differential") Periodic oluion of van der Pol differenial equaion. by A. Arimoo Deparmen of Mahemaic Muahi Iniue of Technology Tokyo Japan in Seminar a Kiami Iniue of Technology January 8 9. Inroducion Le u conider a

Periodic oluion of van der Pol differenial equaion. by A. Arimoo Deparmen of Mahemaic Muahi Iniue of Technology Tokyo Japan in Seminar a Kiami Iniue of Technology January 8 9. Inroducion Le u conider a

ΑΠΟΣΗΜΖΖ ΠΑΡΑΓΩΓΩΝ ΔΤΡΩΠΑΗΚΟΤ ΣΤΠΟΤ (CURRENCY OPTIONS, BINARY OPTIONS, COMPOUND OPTIONS, CHOOSER OPTIONS, LOOKBACK OPTIONS, ASIAN OPTIONS)

") ΑΠΟΣΗΜΖΖ ΠΑΡΑΓΩΓΩΝ ΔΤΡΩΠΑΗΚΟΤ ΣΤΠΟΤ (CURRENCY OPIONS, BINARY OPIONS, COMPOUND OPIONS, CHOOSER OPIONS, LOOKBACK OPIONS, ASIAN OPIONS) ΣΑΝΣΟΤΛΟΤ ΔΛΔΝΖ ΔΠΗΒΛΔΠΩΝ ΚΑΘΖΓΖΣΖ: ΠΖΛΗΩΣΖ ΗΩΑΝΝΖ ΔΘΝΗΚΟ ΜΔΣΟΒΗΟ ΠΟΛΤΣΔΥΝΔΗΟ

ΑΠΟΣΗΜΖΖ ΠΑΡΑΓΩΓΩΝ ΔΤΡΩΠΑΗΚΟΤ ΣΤΠΟΤ (CURRENCY OPIONS, BINARY OPIONS, COMPOUND OPIONS, CHOOSER OPIONS, LOOKBACK OPIONS, ASIAN OPIONS) ΣΑΝΣΟΤΛΟΤ ΔΛΔΝΖ ΔΠΗΒΛΔΠΩΝ ΚΑΘΖΓΖΣΖ: ΠΖΛΗΩΣΖ ΗΩΑΝΝΖ ΔΘΝΗΚΟ ΜΔΣΟΒΗΟ ΠΟΛΤΣΔΥΝΔΗΟ

Necessary and sufficient conditions for oscillation of first order nonlinear neutral differential equations

J. Mah. Anal. Appl. 321 (2006) 553 568 www.elsevier.com/locae/jmaa Necessary sufficien condiions for oscillaion of firs order nonlinear neural differenial equaions X.H. ang a,, Xiaoyan Lin b a School of

J. Mah. Anal. Appl. 321 (2006) 553 568 www.elsevier.com/locae/jmaa Necessary sufficien condiions for oscillaion of firs order nonlinear neural differenial equaions X.H. ang a,, Xiaoyan Lin b a School of

TRM +4!5"2# 6!#!-!2&'!5$27!842//22&'9&2:1*;832<

TRM!"#$%& ' *,-./ *!#!!%!&!3,&!$-!$./!!"#$%&'*" 4!5"# 6!#!-!&'!5$7!84//&'9&:*;83< #:4

TRM!"#$%& ' *,-./ *!#!!%!&!3,&!$-!$./!!"#$%&'*" 4!5"# 6!#!-!&'!5$7!84//&'9&:*;83< #:4

= e 6t. = t 1 = t. 5 t 8L 1[ 1 = 3L 1 [ 1. L 1 [ π. = 3 π. = L 1 3s = L. = 3L 1 s t. = 3 cos(5t) sin(5t).

sin(5t).") Worked Soluion 95 Chaper 25: The Invere Laplace Tranform 25 a From he able: L ] e 6 6 25 c L 2 ] ] L! + 25 e L 5 2 + 25] ] L 5 2 + 5 2 in(5) 252 a L 6 + 2] L 6 ( 2)] 6L ( 2)] 6e 2 252 c L 3 8 4] 3L ] 8L

Worked Soluion 95 Chaper 25: The Invere Laplace Tranform 25 a From he able: L ] e 6 6 25 c L 2 ] ] L! + 25 e L 5 2 + 25] ] L 5 2 + 5 2 in(5) 252 a L 6 + 2] L 6 ( 2)] 6L ( 2)] 6e 2 252 c L 3 8 4] 3L ] 8L

Reservoir modeling. Reservoir modelling Linear reservoirs. The linear reservoir, no input. Starting up reservoir modeling

Reservoir modeling Reservoir modelling Linear reservoirs Paul Torfs Basic equaion for one reservoir:) change in sorage = sum of inflows minus ouflows = Q in,n Q ou,n n n jus an ordinary differenial equaion

Reservoir modeling Reservoir modelling Linear reservoirs Paul Torfs Basic equaion for one reservoir:) change in sorage = sum of inflows minus ouflows = Q in,n Q ou,n n n jus an ordinary differenial equaion

ΕΡΓΑΣΙΑ ΜΑΘΗΜΑΤΟΣ: ΘΕΩΡΙΑ ΒΕΛΤΙΣΤΟΥ ΕΛΕΓΧΟΥ ΦΙΛΤΡΟ KALMAN ΜΩΥΣΗΣ ΛΑΖΑΡΟΣ

ΑΡΙΣΤΟΤΕΛΕΙΟ ΠΑΝΕΠΙΣΤΗΜΙΟ ΘΕΣΣΑΛΟΝΙΚΗΣ ΤΜΗΜΑ ΜΑΘΗΜΑΤΙΚΩΝ ΜΕΤΑΠΤΥΧΙΑΚΟ ΠΡΟΓΡΑΜΜΑ ΣΠΟΥΔΩΝ ΘΕΩΡΗΤΙΚΗ ΠΛΗΡΟΦΟΡΙΚΗ ΚΑΙ ΘΕΩΡΙΑ ΣΥΣΤΗΜΑΤΩΝ & ΕΛΕΓΧΟΥ ΕΡΓΑΣΙΑ ΜΑΘΗΜΑΤΟΣ: ΘΕΩΡΙΑ ΒΕΛΤΙΣΤΟΥ ΕΛΕΓΧΟΥ ΦΙΛΤΡΟ KALMAN ΜΩΥΣΗΣ

ΑΡΙΣΤΟΤΕΛΕΙΟ ΠΑΝΕΠΙΣΤΗΜΙΟ ΘΕΣΣΑΛΟΝΙΚΗΣ ΤΜΗΜΑ ΜΑΘΗΜΑΤΙΚΩΝ ΜΕΤΑΠΤΥΧΙΑΚΟ ΠΡΟΓΡΑΜΜΑ ΣΠΟΥΔΩΝ ΘΕΩΡΗΤΙΚΗ ΠΛΗΡΟΦΟΡΙΚΗ ΚΑΙ ΘΕΩΡΙΑ ΣΥΣΤΗΜΑΤΩΝ & ΕΛΕΓΧΟΥ ΕΡΓΑΣΙΑ ΜΑΘΗΜΑΤΟΣ: ΘΕΩΡΙΑ ΒΕΛΤΙΣΤΟΥ ΕΛΕΓΧΟΥ ΦΙΛΤΡΟ KALMAN ΜΩΥΣΗΣ

Z L L L N b d g 5 * " # $ % $ ' $ % % % ) * + *, - %. / / + 3 / / / / + * 4 / / 1 " 5 % / 6, 7 # * $ 8 2. / / % 1 9 ; < ; = ; ; >? 8 3 " #

* + *, - %. / / + 3 / / / / + * 4 / / 1 5 % / 6, 7 # * $ 8 2. / / % 1 9 ; < ; = ; ; >? 8 3 #") Z L L L N b d g 5 * " # $ % $ ' $ % % % ) * + *, - %. / 0 1 2 / + 3 / / 1 2 3 / / + * 4 / / 1 " 5 % / 6, 7 # * $ 8 2. / / % 1 9 ; < ; = ; ; >? 8 3 " # $ % $ ' $ % ) * % @ + * 1 A B C D E D F 9 O O D H

Z L L L N b d g 5 * " # $ % $ ' $ % % % ) * + *, - %. / 0 1 2 / + 3 / / 1 2 3 / / + * 4 / / 1 " 5 % / 6, 7 # * $ 8 2. / / % 1 9 ; < ; = ; ; >? 8 3 " # $ % $ ' $ % ) * % @ + * 1 A B C D E D F 9 O O D H

Teor imov r. ta matem. statist. Vip. 94, 2016, stor

eor imov r. ta matem. statist. Vip. 94, 6, stor. 93 5 Abstract. e article is devoted to models of financial markets wit stocastic volatility, wic is defined by a functional of Ornstein-Ulenbeck process

eor imov r. ta matem. statist. Vip. 94, 6, stor. 93 5 Abstract. e article is devoted to models of financial markets wit stocastic volatility, wic is defined by a functional of Ornstein-Ulenbeck process

Arbitrage Analysis of Futures Market with Frictions

2007 1 1 :100026788 (2007) 0120033206, (, 200052) : Vignola2Dale (1980) Kawaller2Koch(1984) (cost of carry),.,, ;,, : ;,;,. : ;;; : F83019 : A Arbitrage Analysis of Futures Market with Frictions LIU Hai2long,

2007 1 1 :100026788 (2007) 0120033206, (, 200052) : Vignola2Dale (1980) Kawaller2Koch(1984) (cost of carry),.,, ;,, : ;,;,. : ;;; : F83019 : A Arbitrage Analysis of Futures Market with Frictions LIU Hai2long,

16. 17. r t te 2t i t 1. 18 19 Find the derivative of the vector function. 19. r t e t cos t i e t sin t j ln t k. 31 33 Evaluate the integral.

SECTION.7 VECTOR FUNCTIONS AND SPACE CURVES.7 VECTOR FUNCTIONS AND SPACE CURVES A Click here for answers. S Click here for soluions. Copyrigh Cengage Learning. All righs reserved.. Find he domain of he

SECTION.7 VECTOR FUNCTIONS AND SPACE CURVES.7 VECTOR FUNCTIONS AND SPACE CURVES A Click here for answers. S Click here for soluions. Copyrigh Cengage Learning. All righs reserved.. Find he domain of he

No General Serial No JOURNAL OF XIAMEN UNIVERSITY Arts & Social Sciences CTD F CTD

2015 1 227 JOURNAL OF XIAMEN UNIVERSITY Arts & Social Sciences No. 1 2015 General Serial No. 227 361005 CTD F830. 9 A 0438-0460 2015 01-0033-08 2013 9 6 4 7 CTD 2014-09-10 71101121 71371161 71471155 33

2015 1 227 JOURNAL OF XIAMEN UNIVERSITY Arts & Social Sciences No. 1 2015 General Serial No. 227 361005 CTD F830. 9 A 0438-0460 2015 01-0033-08 2013 9 6 4 7 CTD 2014-09-10 71101121 71371161 71471155 33

WTO. ( Kanamori and Zhao,2006 ;,2006), ,,2005, , , 1114 % 1116 % 1119 %,

, ,,2005, , , 1114 % 1116 % 1119 %,") : 3 :,, (VAR),,, : 997, 200, WTO,, 2005 7 2, 2,, ( Kanamori and Zhao,2006 ;,2006),,, 2005 7 2,,,,, :,,2005, 2007 265,200 0,,,2005 2006 2007, 4 % 6 % 9 %,,,,,,,, 3,, :00836, zhaozhijun @yahoo. com ;,, :25000,

: 3 :,, (VAR),,, : 997, 200, WTO,, 2005 7 2, 2,, ( Kanamori and Zhao,2006 ;,2006),,, 2005 7 2,,,,, :,,2005, 2007 265,200 0,,,2005 2006 2007, 4 % 6 % 9 %,,,,,,,, 3,, :00836, zhaozhijun @yahoo. com ;,, :25000,

Financial Risk Management

Pricing of American options University of Oulu - Department of Finance Spring 2017 Volatility-based binomial price process uuuus 0 = 26.51 uuus 0 = 24.71 uus 0 = us 0 = S 0 = ds 0 = dds 0 = ddds 0 = 16.19

Pricing of American options University of Oulu - Department of Finance Spring 2017 Volatility-based binomial price process uuuus 0 = 26.51 uuus 0 = 24.71 uus 0 = us 0 = S 0 = ds 0 = dds 0 = ddds 0 = 16.19

Analiza reakcji wybranych modeli

Bank i Kredy 43 (4), 202, 85 8 www.bankikredy.nbp.pl www.bankandcredi.nbp.pl Analiza reakcji wybranych modeli 86 - - - srice - - - per capia research and developmen dynamic sochasic general equilibrium

Bank i Kredy 43 (4), 202, 85 8 www.bankikredy.nbp.pl www.bankandcredi.nbp.pl Analiza reakcji wybranych modeli 86 - - - srice - - - per capia research and developmen dynamic sochasic general equilibrium

Mean-Variance Hedging on uncertain time horizon in a market with a jump

Mean-Variance Hedging on uncertain time horizon in a market with a jump Thomas LIM 1 ENSIIE and Laboratoire Analyse et Probabilités d Evry Young Researchers Meeting on BSDEs, Numerics and Finance, Oxford

Mean-Variance Hedging on uncertain time horizon in a market with a jump Thomas LIM 1 ENSIIE and Laboratoire Analyse et Probabilités d Evry Young Researchers Meeting on BSDEs, Numerics and Finance, Oxford

Positive solutions for a multi-point eigenvalue. problem involving the one dimensional

Elecronic Journal of Qualiaive Theory of Differenial Equaions 29, No. 4, -3; h://www.mah.u-szeged.hu/ejqde/ Posiive soluions for a muli-oin eigenvalue roblem involving he one dimensional -Lalacian Youyu

Elecronic Journal of Qualiaive Theory of Differenial Equaions 29, No. 4, -3; h://www.mah.u-szeged.hu/ejqde/ Posiive soluions for a muli-oin eigenvalue roblem involving he one dimensional -Lalacian Youyu

( ) ( ) ( ) ( ) ( ) 槡 槡 槡 ( ) 槡 槡 槡 槡 ( ) ( )

( ) ( ) ( ) ( ) 槡 槡 槡 ( ) 槡 槡 槡 槡 ( ) ( )") 3 3 Vol.3.3 0 3 JournalofHarbinEngineeringUniversity Mar.0 doi:0.3969/j.isn.006-7043.0.03.0 ARIMA GARCH,, 5000 :!""#$%&' *+&,$-.,/0 ' 3$,456$*+7&'89 $:;,/0 ?4@A$ ARI MA GARCHBCDE FG%&HIJKL$ B

3 3 Vol.3.3 0 3 JournalofHarbinEngineeringUniversity Mar.0 doi:0.3969/j.isn.006-7043.0.03.0 ARIMA GARCH,, 5000 :!""#$%&' *+&,$-.,/0 ' 3$,456$*+7&'89 $:;,/0 ?4@A$ ARI MA GARCHBCDE FG%&HIJKL$ B

Ó³ Ÿ , º 2(214).. 171Ä176. Š Œ œ ƒˆˆ ˆ ˆŠ

.. 171Ä176. Š Œ œ ƒˆˆ ˆ ˆŠ") Ó³ Ÿ. 218.. 15, º 2(214).. 171Ä176 Š Œ œ ƒˆˆ ˆ ˆŠ ˆ ˆ ˆ Š Š Œ Œ Ÿ ˆ Š ˆ Š ˆ ˆŠ Œ œ ˆ.. Š Ö,, 1,.. ˆ μ,,.. μ³ μ,.. ÉÓÖ μ,,.š. ʳÖ,, Í μ ²Ó Ò ² μ É ²Ó ± Ö Ò Ê É É Œˆ ˆ, Œμ ± Ñ Ò É ÉÊÉ Ö ÒÌ ² μ, Ê μ ± Ê É

Ó³ Ÿ. 218.. 15, º 2(214).. 171Ä176 Š Œ œ ƒˆˆ ˆ ˆŠ ˆ ˆ ˆ Š Š Œ Œ Ÿ ˆ Š ˆ Š ˆ ˆŠ Œ œ ˆ.. Š Ö,, 1,.. ˆ μ,,.. μ³ μ,.. ÉÓÖ μ,,.š. ʳÖ,, Í μ ²Ó Ò ² μ É ²Ó ± Ö Ò Ê É É Œˆ ˆ, Œμ ± Ñ Ò É ÉÊÉ Ö ÒÌ ² μ, Ê μ ± Ê É

Non-Markovian dynamics of an open quantum system in fermionic environments

Non-Marovian dynamics of an open quanum sysem in fermionic environmens J. Q. You Deparmen of Physics, Fudan Universiy, Shanghai, and Beijing Compuaional Science Research Cener, Beijing Mi Chen (PhD suden

Non-Marovian dynamics of an open quanum sysem in fermionic environmens J. Q. You Deparmen of Physics, Fudan Universiy, Shanghai, and Beijing Compuaional Science Research Cener, Beijing Mi Chen (PhD suden

The Student s t and F Distributions Page 1

The Suden s and F Disribuions Page The Fundamenal Transformaion formula for wo random variables: Consider wo random variables wih join probabiliy disribuion funcion f (, ) simulaneously ake on values in

The Suden s and F Disribuions Page The Fundamenal Transformaion formula for wo random variables: Consider wo random variables wih join probabiliy disribuion funcion f (, ) simulaneously ake on values in

ΑΝΕΛΙΞΕΙΣ LÉVY: ΘΕΩΡΙΑ & ΕΦΑΡΜΟΓΕΣ ΣΤΑ ΧΡΗΜΑΤΟΟΙΚΟΝΟΜΙΚΑ

ΠΑΝΕΠΙΣΤΗΜΙΟ ΠΕΙΡΑΙΩΣ ΤΜΗΜΑ ΣΤΑΤΙΣΤΙΚΗΣ ΚΑΙ ΑΣΦΑΛΙΣΤΙΚΗΣ ΕΠΙΣΤΗΜΗΣ ΜΕΤΑΠΤΥΧΙΑΚΟ ΠΡΟΓΡΑΜΜΑ ΣΠΟΥ ΩΝ ΣΤΗΝ ΕΦΑΡΜΟΣΜΕΝΗ ΣΤΑΤΙΣΤΙΚΗ ΑΝΕΛΙΞΕΙΣ LÉVY: ΘΕΩΡΙΑ & ΕΦΑΡΜΟΓΕΣ ΣΤΑ ΧΡΗΜΑΤΟΟΙΚΟΝΟΜΙΚΑ Ιωάννης. Μίχας ιπλωµατική

ΠΑΝΕΠΙΣΤΗΜΙΟ ΠΕΙΡΑΙΩΣ ΤΜΗΜΑ ΣΤΑΤΙΣΤΙΚΗΣ ΚΑΙ ΑΣΦΑΛΙΣΤΙΚΗΣ ΕΠΙΣΤΗΜΗΣ ΜΕΤΑΠΤΥΧΙΑΚΟ ΠΡΟΓΡΑΜΜΑ ΣΠΟΥ ΩΝ ΣΤΗΝ ΕΦΑΡΜΟΣΜΕΝΗ ΣΤΑΤΙΣΤΙΚΗ ΑΝΕΛΙΞΕΙΣ LÉVY: ΘΕΩΡΙΑ & ΕΦΑΡΜΟΓΕΣ ΣΤΑ ΧΡΗΜΑΤΟΟΙΚΟΝΟΜΙΚΑ Ιωάννης. Μίχας ιπλωµατική

, 11 1 / 49

ÍÚÈÔ (È È È Ï Ê Ø2017 ÏÑ) Ñ(1) È 2017 10 4, 11 1 / 49 ÏÑÒ ØËÌÙ Õ Õ Ø 2 / 49 ÏÑÒ ØËÌÙ ÏÑÒ ØËÌÙ Õ Õ Ø (I) Í(Ù ) ØÙ Ù ÚÓ (II) Black-Scholes-Merton Ð Ú ÌÑØÎÔ Ð Ô Black-Scholes (III) ØÕÊÔ ÕÚÔÍ(ÓÙÊØ Ú ) È ÎÑØÎÔ

ÍÚÈÔ (È È È Ï Ê Ø2017 ÏÑ) Ñ(1) È 2017 10 4, 11 1 / 49 ÏÑÒ ØËÌÙ Õ Õ Ø 2 / 49 ÏÑÒ ØËÌÙ ÏÑÒ ØËÌÙ Õ Õ Ø (I) Í(Ù ) ØÙ Ù ÚÓ (II) Black-Scholes-Merton Ð Ú ÌÑØÎÔ Ð Ô Black-Scholes (III) ØÕÊÔ ÕÚÔÍ(ÓÙÊØ Ú ) È ÎÑØÎÔ

Study of limit cycles for some non-smooth Liénard systems

3 011 5 ( ) Journal of East China Normal University (Natural Science) No. 3 May 011 Article ID: 1000-5641(011)03-0044-10 Study of limit cycles for some non-smooth Liénard systems YANG Lu, LIU Xia, XING

3 011 5 ( ) Journal of East China Normal University (Natural Science) No. 3 May 011 Article ID: 1000-5641(011)03-0044-10 Study of limit cycles for some non-smooth Liénard systems YANG Lu, LIU Xia, XING

90 [, ] p Panel nested error structure) : Lagrange-multiple LM) Honda [3] LM ; King Wu, Baltagi, Chang Li [4] Moulton Randolph ANOVA) F p Panel,, p Z

![90 [, ] p Panel nested error structure) : Lagrange-multiple LM) Honda [3] LM ; King Wu, Baltagi, Chang Li [4] Moulton Randolph ANOVA) F p Panel,, p Z](/thumbs/91/107678282.jpg "90 [, ] p Panel nested error structure) : Lagrange-multiple LM) Honda [3] LM ; King Wu, Baltagi, Chang Li [4] Moulton Randolph ANOVA) F p Panel,, p Z") 00 Chinese Journal of Applied Probability and Statistics Vol6 No Feb 00 Panel, 3,, 0034;,, 38000) 3,, 000) p Panel,, p Panel : Panel,, p,, : O,,, nuisance parameter), Tsui Weerahandi [] Weerahandi [] p

00 Chinese Journal of Applied Probability and Statistics Vol6 No Feb 00 Panel, 3,, 0034;,, 38000) 3,, 000) p Panel,, p Panel : Panel,, p,, : O,,, nuisance parameter), Tsui Weerahandi [] Weerahandi [] p

Optimizing Microwave-assisted Extraction Process for Paprika Red Pigments Using Response Surface Methodology

2012 34 2 382-387 http / /xuebao. jxau. edu. cn Acta Agriculturae Universitatis Jiangxiensis E - mail ndxb7775@ sina. com 212018 105 W 42 2 min 0. 631 TS202. 3 A 1000-2286 2012 02-0382 - 06 Optimizing

2012 34 2 382-387 http / /xuebao. jxau. edu. cn Acta Agriculturae Universitatis Jiangxiensis E - mail ndxb7775@ sina. com 212018 105 W 42 2 min 0. 631 TS202. 3 A 1000-2286 2012 02-0382 - 06 Optimizing

P13-2014-14. .. ²ÒÏ 1,,.Š. μ μ 1, 2, 1, 3, ,. ʳÌÊÊ. Œ œ ˆ ŒˆŠˆ ˆŒ œ ƒ Š ˆ -2Œ ˆ Š Œ ˆ ˆ Œ ˆŸ Œ ˆ. ² μ Ê ² Annals of Nuclear Energy

P13-2014-14.. ²ÒÏ 1,,.Š. μ μ 1, 2, 1, 3,,. ʳÌÊÊ Œ œ ˆ ŒˆŠˆ ˆŒ œ ƒ Š ˆ -2Œ Ÿ ˆ ˆŸ ˆ Š Œ ˆ ˆ Œ ˆŸ Œ ˆ ² μ Ê ² Annals of Nuclear Energy 1 Ñ Ò É ÉÊÉ Ö ÒÌ ² μ, Ê 2 ² ² Œƒ Œˆ, Ê, μ Ö 3 ˆ É ÉÊÉ Ë ± É Ì μ²μ Œ,

P13-2014-14.. ²ÒÏ 1,,.Š. μ μ 1, 2, 1, 3,,. ʳÌÊÊ Œ œ ˆ ŒˆŠˆ ˆŒ œ ƒ Š ˆ -2Œ Ÿ ˆ ˆŸ ˆ Š Œ ˆ ˆ Œ ˆŸ Œ ˆ ² μ Ê ² Annals of Nuclear Energy 1 Ñ Ò É ÉÊÉ Ö ÒÌ ² μ, Ê 2 ² ² Œƒ Œˆ, Ê, μ Ö 3 ˆ É ÉÊÉ Ë ± É Ì μ²μ Œ,

SOLUTIONS TO MATH38181 EXTREME VALUES AND FINANCIAL RISK EXAM

SOLUTIONS TO MATH38181 EXTREME VALUES AND FINANCIAL RISK EXAM Solutions to Question 1 a) The cumulative distribution function of T conditional on N n is Pr T t N n) Pr max X 1,..., X N ) t N n) Pr max

SOLUTIONS TO MATH38181 EXTREME VALUES AND FINANCIAL RISK EXAM Solutions to Question 1 a) The cumulative distribution function of T conditional on N n is Pr T t N n) Pr max X 1,..., X N ) t N n) Pr max

! " # $ % & $ % & $ & # " ' $ ( $ ) * ) * +, -. / # $ $ ( $ " $ $ $ % $ $ ' ƒ " " ' %. " 0 1 2 3 4 5 6 7 8 9 : ; ; < = : ; > : 0? @ 8? 4 A 1 4 B 3 C 8? D C B? E F 4 5 8 3 G @ H I@ A 1 4 D G 8 5 1 @ J C

! " # $ % & $ % & $ & # " ' $ ( $ ) * ) * +, -. / # $ $ ( $ " $ $ $ % $ $ ' ƒ " " ' %. " 0 1 2 3 4 5 6 7 8 9 : ; ; < = : ; > : 0? @ 8? 4 A 1 4 B 3 C 8? D C B? E F 4 5 8 3 G @ H I@ A 1 4 D G 8 5 1 @ J C

) * +, -. + / - 0 1 2 3 4 5 6 7 8 9 6 : ; < 8 = 8 9 >? @ A 4 5 6 7 8 9 6 ; = B? @ : C B B D 9 E : F 9 C 6 < G 8 B A F A > < C 6 < B H 8 9 I 8 9 E ) * +, -. + / J - 0 1 2 3 J K 3 L M N L O / 1 L 3 O 2,

) * +, -. + / - 0 1 2 3 4 5 6 7 8 9 6 : ; < 8 = 8 9 >? @ A 4 5 6 7 8 9 6 ; = B? @ : C B B D 9 E : F 9 C 6 < G 8 B A F A > < C 6 < B H 8 9 I 8 9 E ) * +, -. + / J - 0 1 2 3 J K 3 L M N L O / 1 L 3 O 2,

Theory and Effectiveness Evaluation of the Chinese Government s Intervention in the Housing Market

28 1 2011 1 Saisical Research Vol. 28 No. 1 Jan. 2011 2003 6 2005 2006 2004 C812 A 1002-4565 2011 01-0027 - 09 Theory and Effeciveness Evaluaion of he Chinese Governmen s Inervenion in he Housing Marke

28 1 2011 1 Saisical Research Vol. 28 No. 1 Jan. 2011 2003 6 2005 2006 2004 C812 A 1002-4565 2011 01-0027 - 09 Theory and Effeciveness Evaluaion of he Chinese Governmen s Inervenion in he Housing Marke

Cointegrated Commodity Pricing Model

Coinegraed Commodiy Pricing Model Kasushi Nakajima and Kazuhiko Ohashi Firs draf: December 20, 2008 This draf: April 9, 2009 Absrac In his paper, we propose a commodiy pricing model ha exends Gibson-Schwarz

Coinegraed Commodiy Pricing Model Kasushi Nakajima and Kazuhiko Ohashi Firs draf: December 20, 2008 This draf: April 9, 2009 Absrac In his paper, we propose a commodiy pricing model ha exends Gibson-Schwarz

Αλγοριθμική ασυμπτωτική ανάλυση πεπερασμένης αργής πολλαπλότητας: O ελκυστής Rössler

EΘΝΙΚΟ ΜΕΤΣΟΒΕΙΟ ΠΟΛΥΤΕΧΝΕΙΟ ΣΧΟΛΗ ΕΦΑΡΜΟΣΜΕΝΩΝ ΜΑΘΗΜΑΤΙΚΩΝ ΚΑΙ ΦΥΣΙΚΩΝ ΕΠΙΣΤΗΜΩΝ ΔΙΠΛΩΜΑΤΙΚΗ ΕΡΓΑΣΙΑ Αλγοριθμική ασυμπτωτική ανάλυση πεπερασμένης αργής πολλαπλότητας: O ελκυστής Rössler Συντάκτης: ΜΑΡΗΣ

EΘΝΙΚΟ ΜΕΤΣΟΒΕΙΟ ΠΟΛΥΤΕΧΝΕΙΟ ΣΧΟΛΗ ΕΦΑΡΜΟΣΜΕΝΩΝ ΜΑΘΗΜΑΤΙΚΩΝ ΚΑΙ ΦΥΣΙΚΩΝ ΕΠΙΣΤΗΜΩΝ ΔΙΠΛΩΜΑΤΙΚΗ ΕΡΓΑΣΙΑ Αλγοριθμική ασυμπτωτική ανάλυση πεπερασμένης αργής πολλαπλότητας: O ελκυστής Rössler Συντάκτης: ΜΑΡΗΣ

P AND P. P : actual probability. P : risk neutral probability. Realtionship: mutual absolute continuity P P. For example:

(B t, S (t) t P AND P,..., S (p) t ): securities P : actual probability P : risk neutral probability Realtionship: mutual absolute continuity P P For example: P : ds t = µ t S t dt + σ t S t dw t P : ds

(B t, S (t) t P AND P,..., S (p) t ): securities P : actual probability P : risk neutral probability Realtionship: mutual absolute continuity P P For example: P : ds t = µ t S t dt + σ t S t dw t P : ds

ACTA MATHEMATICAE APPLICATAE SINICA Sep., ( MR (2000) Õ È 32C17; 32F07; 35G30; 53C55

Õ È 32C17; 32F07; 35G30; 53C55") 37 5 Ó Ä Ä Vol. 37 No. 5 014 9 ACTA MATHEMATICAE APPLICATAE SINICA Sep., 014 É Ì - Î Dirichle ÓÆ ÞÝÜ ÎÞÈÅÔÅ ÅÅ 100048 E-mail: wyin@mail.cnu.edu.cn Ñ - ƱРÑĐ» ³Æ Ð Û Ò ÌĐ Ø ÕÃ Ý Caran-Harogs ÚÆ - ƱРDirichle

37 5 Ó Ä Ä Vol. 37 No. 5 014 9 ACTA MATHEMATICAE APPLICATAE SINICA Sep., 014 É Ì - Î Dirichle ÓÆ ÞÝÜ ÎÞÈÅÔÅ ÅÅ 100048 E-mail: wyin@mail.cnu.edu.cn Ñ - ƱРÑĐ» ³Æ Ð Û Ò ÌĐ Ø ÕÃ Ý Caran-Harogs ÚÆ - ƱРDirichle

: Monte Carlo EM 313, Louis (1982) EM, EM Newton-Raphson, /. EM, 2 Monte Carlo EM Newton-Raphson, Monte Carlo EM, Monte Carlo EM, /. 3, Monte Carlo EM

EM, EM Newton-Raphson, /. EM, 2 Monte Carlo EM Newton-Raphson, Monte Carlo EM, Monte Carlo EM, /. 3, Monte Carlo EM") 2008 6 Chinese Journal of Applied Probability and Statistics Vol.24 No.3 Jun. 2008 Monte Carlo EM 1,2 ( 1,, 200241; 2,, 310018) EM, E,,. Monte Carlo EM, EM E Monte Carlo,. EM, Monte Carlo EM,,,,. Newton-Raphson.

2008 6 Chinese Journal of Applied Probability and Statistics Vol.24 No.3 Jun. 2008 Monte Carlo EM 1,2 ( 1,, 200241; 2,, 310018) EM, E,,. Monte Carlo EM, EM E Monte Carlo,. EM, Monte Carlo EM,,,,. Newton-Raphson.

Nov Journal of Zhengzhou University Engineering Science Vol. 36 No FCM. A doi /j. issn

2015 11 Nov 2015 36 6 Journal of Zhengzhou University Engineering Science Vol 36 No 6 1671-6833 2015 06-0056 - 05 C 1 1 2 2 1 450001 2 461000 C FCM FCM MIA MDC MDC MIA I FCM c FCM m FCM C TP18 A doi 10

2015 11 Nov 2015 36 6 Journal of Zhengzhou University Engineering Science Vol 36 No 6 1671-6833 2015 06-0056 - 05 C 1 1 2 2 1 450001 2 461000 C FCM FCM MIA MDC MDC MIA I FCM c FCM m FCM C TP18 A doi 10

Adaptive grouping difference variation wolf pack algorithm

3 2017 5 ( ) Journal of East China Normal University (Natural Science) No. 3 May 2017 : 1000-5641(2017)03-0078-09, (, 163318) :,,.,,,,.,,. : ; ; ; : TP301.6 : A DOI: 10.3969/j.issn.1000-5641.2017.03.008

3 2017 5 ( ) Journal of East China Normal University (Natural Science) No. 3 May 2017 : 1000-5641(2017)03-0078-09, (, 163318) :,,.,,,,.,,. : ; ; ; : TP301.6 : A DOI: 10.3969/j.issn.1000-5641.2017.03.008

(1) P(Ω) = 1. i=1 A i) = i=1 P(A i)

P(Ω) = 1. i=1 A i) = i=1 P(A i)") Χρηματοοικονομικά Μαθηματικά Το συνεχές μοντέλο συνεχούς χρόνου Σ. Ξανθόπουλος Παν. Αιγαίου Χειμερινό Εξάμηνο 2015-2016 Χειμερινό Εξάμηνο 2015-2016 1 / Σύνοψη 1 Προκαταρκτικά 2 Διαδικασία Wiener ή Κίνηση

Χρηματοοικονομικά Μαθηματικά Το συνεχές μοντέλο συνεχούς χρόνου Σ. Ξανθόπουλος Παν. Αιγαίου Χειμερινό Εξάμηνο 2015-2016 Χειμερινό Εξάμηνο 2015-2016 1 / Σύνοψη 1 Προκαταρκτικά 2 Διαδικασία Wiener ή Κίνηση

Motion analysis and simulation of a stratospheric airship

32 11 Vol 32 11 2011 11 Journal of Harbin Engineering University Nov 2011 doi 10 3969 /j issn 1006-7043 2011 11 019 410073 3 2 V274 A 1006-7043 2011 11-1501-08 Motion analysis and simulation of a stratospheric

32 11 Vol 32 11 2011 11 Journal of Harbin Engineering University Nov 2011 doi 10 3969 /j issn 1006-7043 2011 11 019 410073 3 2 V274 A 1006-7043 2011 11-1501-08 Motion analysis and simulation of a stratospheric

Financial Risk Management

Pricing of American options University of Oulu - Department of Finance Spring 2018 Volatility-based binomial price process uuuus 0 = 26.51 uuus 0 = 24.71 uus 0 = us 0 = S 0 = ds 0 = dds 0 = ddds 0 = 16.19

Pricing of American options University of Oulu - Department of Finance Spring 2018 Volatility-based binomial price process uuuus 0 = 26.51 uuus 0 = 24.71 uus 0 = us 0 = S 0 = ds 0 = dds 0 = ddds 0 = 16.19

Appendix A. Stability of the logistic semi-discrete model.

Ecological Archiv E89-7-A Elizava Pachpky, Rogr M. Nib, and William W. Murdoch. 8. Bwn dicr and coninuou: conumr-rourc dynamic wih ynchronizd rproducion. Ecology 89:8-88. Appndix A. Sabiliy of h logiic

Ecological Archiv E89-7-A Elizava Pachpky, Rogr M. Nib, and William W. Murdoch. 8. Bwn dicr and coninuou: conumr-rourc dynamic wih ynchronizd rproducion. Ecology 89:8-88. Appndix A. Sabiliy of h logiic

University of Washington Department of Chemistry Chemistry 553 Spring Quarter 2010 Homework Assignment 3 Due 04/26/10

Universiy of Washingon Deparmen of Chemisry Chemisry 553 Spring Quarer 1 Homework Assignmen 3 Due 4/6/1 v e v e A s ds: a) Show ha for large 1 and, (i.e. 1 >> and >>) he velociy auocorrelaion funcion 1)

Universiy of Washingon Deparmen of Chemisry Chemisry 553 Spring Quarer 1 Homework Assignmen 3 Due 4/6/1 v e v e A s ds: a) Show ha for large 1 and, (i.e. 1 >> and >>) he velociy auocorrelaion funcion 1)

Vol. 34 ( 2014 ) No. 4. J. of Math. (PRC) : A : (2014) XJ130246).

No. 4. J. of Math. (PRC) : A : (2014) XJ130246).") Vol. 34 ( 2014 ) No. 4 J. of Math. (PRC) (, 710123) :. -,,, [8].,,. : ; - ; ; MR(2010) : 91A30; 91B30 : O225 : A : 0255-7797(2014)04-0779-08 1,. [1],. [2],.,,,. [3],.,,,.,,,,.., [4].,.. [5] -,. [6] Markov.

Vol. 34 ( 2014 ) No. 4 J. of Math. (PRC) (, 710123) :. -,,, [8].,,. : ; - ; ; MR(2010) : 91A30; 91B30 : O225 : A : 0255-7797(2014)04-0779-08 1,. [1],. [2],.,,,. [3],.,,,.,,,,.., [4].,.. [5] -,. [6] Markov.

Nonlinear Analysis: Modelling and Control, 2013, Vol. 18, No. 4,

Nonlinear Analysis: Modelling and Conrol, 23, Vol. 8, No. 4, 493 58 493 Exisence and uniqueness of soluions for a singular sysem of higher-order nonlinear fracional differenial equaions wih inegral boundary

Nonlinear Analysis: Modelling and Conrol, 23, Vol. 8, No. 4, 493 58 493 Exisence and uniqueness of soluions for a singular sysem of higher-order nonlinear fracional differenial equaions wih inegral boundary

Riemann Hypothesis: a GGC representation

Riemann Hypohesis: a GGC represenaion Nicholas G. Polson Universiy of Chicago Augus 8, 8 Absrac A GGC Generalized Gamma Convoluion represenaion for Riemann s reciprocal ξ-funcion is consruced. This provides

Riemann Hypohesis: a GGC represenaion Nicholas G. Polson Universiy of Chicago Augus 8, 8 Absrac A GGC Generalized Gamma Convoluion represenaion for Riemann s reciprocal ξ-funcion is consruced. This provides

Decision making under model uncertainty: Hamilton-Jacobi-Belman-Isaacs approach, weak solutions and applications in Economics and Finance

Βιογραφικό Σημείωμα Ιωάννης Μπαλτάς (Τελευταία Ενημέρωση: Φεβρουάριος, 2017) Προσωπικά Στοιχεία Επίθετο : Μπαλτάς Ονομα : Ιωάννης Υπηκοότητα : Ελληνική Ημερομηνία γεννήσεως : 22 Οκτωβρίου 1983 Τόπος γεννήσεως

Βιογραφικό Σημείωμα Ιωάννης Μπαλτάς (Τελευταία Ενημέρωση: Φεβρουάριος, 2017) Προσωπικά Στοιχεία Επίθετο : Μπαλτάς Ονομα : Ιωάννης Υπηκοότητα : Ελληνική Ημερομηνία γεννήσεως : 22 Οκτωβρίου 1983 Τόπος γεννήσεως

2002 Journal of Software

1000-9825/2002/13(02)0239-06 2002 Journal of Sofware Vol13, No2 -,, (, 100084) E-mail: shijing@mailssinghuaeducn; xingcx@singhuaeducn; dcszlz@singhuaeducn hp://dbgroupcssinghuaeducn : 10 12,, I/O -, -,,,

1000-9825/2002/13(02)0239-06 2002 Journal of Sofware Vol13, No2 -,, (, 100084) E-mail: shijing@mailssinghuaeducn; xingcx@singhuaeducn; dcszlz@singhuaeducn hp://dbgroupcssinghuaeducn : 10 12,, I/O -, -,,,

ER-Tree (Extended R*-Tree)

") 1-9825/22/13(4)768-6 22 Journal of Software Vol13, No4 1, 1, 2, 1 1, 1 (, 2327) 2 (, 3127) E-mail xhzhou@ustceducn,,,,,,, 1, TP311 A,,,, Elias s Rivest,Cleary Arya Mount [1] O(2 d ) Arya Mount [1] Friedman,Bentley

1-9825/22/13(4)768-6 22 Journal of Software Vol13, No4 1, 1, 2, 1 1, 1 (, 2327) 2 (, 3127) E-mail xhzhou@ustceducn,,,,,,, 1, TP311 A,,,, Elias s Rivest,Cleary Arya Mount [1] O(2 d ) Arya Mount [1] Friedman,Bentley

On shift Harnack inequalities for subordinate semigroups and moment estimates for Lévy processes

Available online a www.sciencedirec.com ScienceDirec Sochasic Processes and heir Applicaions 15 (15) 3851 3878 www.elsevier.com/locae/spa On shif Harnack inequaliies for subordinae semigroups and momen

Available online a www.sciencedirec.com ScienceDirec Sochasic Processes and heir Applicaions 15 (15) 3851 3878 www.elsevier.com/locae/spa On shif Harnack inequaliies for subordinae semigroups and momen

Solutions - Chapter 4

Solutions - Chapter Kevin S. Huang Problem.1 Unitary: Ût = 1 ī hĥt Û tût = 1 Neglect t term: 1 + hĥ ī t 1 īhĥt = 1 + hĥ ī t ī hĥt = 1 Ĥ = Ĥ Problem. Ût = lim 1 ī ] n hĥ1t 1 ī ] hĥt... 1 ī ] hĥnt 1 ī ]

Solutions - Chapter Kevin S. Huang Problem.1 Unitary: Ût = 1 ī hĥt Û tût = 1 Neglect t term: 1 + hĥ ī t 1 īhĥt = 1 + hĥ ī t ī hĥt = 1 Ĥ = Ĥ Problem. Ût = lim 1 ī ] n hĥ1t 1 ī ] hĥt... 1 ī ] hĥnt 1 ī ]

P É Ô Ô² 1,2,.. Ò± 1,.. ±μ 1,. ƒ. ±μ μ 1,.Š. ±μ μ 1, ˆ.. Ê Ò 1,.. Ê Ò 1 Œˆ ˆŸ. ² μ Ê ² μ Ì μ ÉÓ. É μ ±, Ì μé μ Ò É μ Ò ² μ Ö

P11-2015-60. É Ô Ô² 1,2,.. Ò± 1,.. ±μ 1,. ƒ. ±μ μ 1,.Š. ±μ μ 1, ˆ.. Ê Ò 1,.. Ê Ò 1 Œ Œ ˆ Š Œ ˆ ˆ Œˆ ˆŸ ƒ Š ˆŒ Š ² μ Ê ² μ Ì μ ÉÓ. É μ ±, Ì μé μ Ò É μ Ò ² μ Ö 1 Ñ Ò É ÉÊÉ Ö ÒÌ ² μ, Ê 2 Œμ μ²ó ± μ Ê É Ò

P11-2015-60. É Ô Ô² 1,2,.. Ò± 1,.. ±μ 1,. ƒ. ±μ μ 1,.Š. ±μ μ 1, ˆ.. Ê Ò 1,.. Ê Ò 1 Œ Œ ˆ Š Œ ˆ ˆ Œˆ ˆŸ ƒ Š ˆŒ Š ² μ Ê ² μ Ì μ ÉÓ. É μ ±, Ì μé μ Ò É μ Ò ² μ Ö 1 Ñ Ò É ÉÊÉ Ö ÒÌ ² μ, Ê 2 Œμ μ²ó ± μ Ê É Ò

Key Formulas From Larson/Farber Elementary Statistics: Picturing the World, Second Edition 2002 Prentice Hall

64_INS.qxd /6/0 :56 AM Page Key Formulas From Larson/Farber Elemenary Saisics: Picuring he World, Second Ediion 00 Prenice Hall CHAPTER Class Widh = round up o nex convenien number Maximum daa enry - Minimum

64_INS.qxd /6/0 :56 AM Page Key Formulas From Larson/Farber Elemenary Saisics: Picuring he World, Second Ediion 00 Prenice Hall CHAPTER Class Widh = round up o nex convenien number Maximum daa enry - Minimum

A research on the influence of dummy activity on float in an AOA network and its amendments

2008 6 6 :100026788 (2008) 0620106209,, (, 102206) : NP2hard,,..,.,,.,.,. :,,,, : TB11411 : A A research on the influence of dummy activity on float in an AOA network and its amendments WANG Qiang, LI

2008 6 6 :100026788 (2008) 0620106209,, (, 102206) : NP2hard,,..,.,,.,.,. :,,,, : TB11411 : A A research on the influence of dummy activity on float in an AOA network and its amendments WANG Qiang, LI

Oscillation criteria for two-dimensional system of non-linear ordinary differential equations

Elecronic Journal of Qualiaive Theory of Differenial Equaions 216, No. 52, 1 17; doi: 1.14232/ejqde.216.1.52 hp://www.mah.u-szeged.hu/ejqde/ Oscillaion crieria for wo-dimensional sysem of non-linear ordinary

Elecronic Journal of Qualiaive Theory of Differenial Equaions 216, No. 52, 1 17; doi: 1.14232/ejqde.216.1.52 hp://www.mah.u-szeged.hu/ejqde/ Oscillaion crieria for wo-dimensional sysem of non-linear ordinary

4.6 Autoregressive Moving Average Model ARMA(1,1)

") 84 CHAPTER 4. STATIONARY TS MODELS 4.6 Autoregressive Moving Average Model ARMA(,) This section is an introduction to a wide class of models ARMA(p,q) which we will consider in more detail later in this

84 CHAPTER 4. STATIONARY TS MODELS 4.6 Autoregressive Moving Average Model ARMA(,) This section is an introduction to a wide class of models ARMA(p,q) which we will consider in more detail later in this

Web-based supplementary materials for Bayesian Quantile Regression for Ordinal Longitudinal Data

Web-based supplementary materials for Bayesian Quantile Regression for Ordinal Longitudinal Data Rahim Alhamzawi, Haithem Taha Mohammad Ali Department of Statistics, College of Administration and Economics,

Web-based supplementary materials for Bayesian Quantile Regression for Ordinal Longitudinal Data Rahim Alhamzawi, Haithem Taha Mohammad Ali Department of Statistics, College of Administration and Economics,

Analysis of optimal harvesting of a prey-predator fishery model with the limited sources of prey and presence of toxicity

ES Web of Confeences 7, 68 (8) hps://doiog/5/esconf/8768 ICEIS 8 nalsis of opimal havesing of a pe-pedao fishe model wih he limied souces of pe and pesence of oici Suimin,, Sii Khabibah, and Dia nies Munawwaoh

ES Web of Confeences 7, 68 (8) hps://doiog/5/esconf/8768 ICEIS 8 nalsis of opimal havesing of a pe-pedao fishe model wih he limied souces of pe and pesence of oici Suimin,, Sii Khabibah, and Dia nies Munawwaoh

On Strong Product of Two Fuzzy Graphs

Inernaional Journal of Scienific and Research Publicaions, Volume 4, Issue 10, Ocober 014 1 ISSN 50-3153 On Srong Produc of Two Fuzzy Graphs Dr. K. Radha* Mr.S. Arumugam** * P.G & Research Deparmen of

Inernaional Journal of Scienific and Research Publicaions, Volume 4, Issue 10, Ocober 014 1 ISSN 50-3153 On Srong Produc of Two Fuzzy Graphs Dr. K. Radha* Mr.S. Arumugam** * P.G & Research Deparmen of

Blowup of regular solutions for radial relativistic Euler equations with damping

8 9 Ö 3 3 Sept. 8 Communication on Applied Mathematics and Computation Vol.3 No.3 DOI.3969/j.issn.6-633.8.3.7 Õ Îµ Ï̺ Eule»²Ö µ ÝÙÚ ÛÞ ØßÜ ( Ñ É ÉÕ Ñ 444 Î ÇÄ Eule ± Æà ¼ Û Â Þ Û ¾ ³ ÇÄ Eule ± Å Å Þ Å

8 9 Ö 3 3 Sept. 8 Communication on Applied Mathematics and Computation Vol.3 No.3 DOI.3969/j.issn.6-633.8.3.7 Õ Îµ Ï̺ Eule»²Ö µ ÝÙÚ ÛÞ ØßÜ ( Ñ É ÉÕ Ñ 444 Î ÇÄ Eule ± Æà ¼ Û Â Þ Û ¾ ³ ÇÄ Eule ± Å Å Þ Å

Ó³ Ÿ , º 7(163).. 755Ä764 ˆ ˆŠ ˆ ˆŠ Š ˆ .. ± Î,. ˆ. ³. ƒ ˆ, Œμ ±

.. 755Ä764 ˆ ˆŠ ˆ ˆŠ Š ˆ .. ± Î,. ˆ. ³. ƒ ˆ, Œμ ±") Ó³ Ÿ. 2010.. 7, º 7(163).. 755Ä764 ˆ ˆŠ ˆ ˆŠ Š ˆ ˆ ƒ ˆ Šˆ ˆ ˆ ƒ Š.. ± Î,. ˆ. ³ ƒ ˆ, Œμ ± μí Ê μ ± É μ μ Êα Î ÉμÉ É É μ ÒÌ ±μ² Î É Í ³ Ö- É Ö - μ É Ì μé±²μ Ö μ ³ Ê²Ó Ê ( ² Î Ì μ³ É Î μ É ) ³ Ö ±Ê²μ- μ

Ó³ Ÿ. 2010.. 7, º 7(163).. 755Ä764 ˆ ˆŠ ˆ ˆŠ Š ˆ ˆ ƒ ˆ Šˆ ˆ ˆ ƒ Š.. ± Î,. ˆ. ³ ƒ ˆ, Œμ ± μí Ê μ ± É μ μ Êα Î ÉμÉ É É μ ÒÌ ±μ² Î É Í ³ Ö- É Ö - μ É Ì μé±²μ Ö μ ³ Ê²Ó Ê ( ² Î Ì μ³ É Î μ É ) ³ Ö ±Ê²μ- μ

Markov chains model reduction

Markov chains model reduction C. Landim Seminar on Stochastic Processes 216 Department of Mathematics University of Maryland, College Park, MD C. Landim Markov chains model reduction March 17, 216 1 /

Markov chains model reduction C. Landim Seminar on Stochastic Processes 216 Department of Mathematics University of Maryland, College Park, MD C. Landim Markov chains model reduction March 17, 216 1 /

552 Lee (2006),,, BIC,. : ; ; ;. 2., Poisson (Zero-Inflated Poisson Distribution), ZIP. Y ZIP(φ, λ), φ + (1 φ) exp( λ), y = 0; P {Y = y} = (1 φ) exp(

,,, BIC,. : ; ; ;. 2., Poisson (Zero-Inflated Poisson Distribution), ZIP. Y ZIP(φ, λ), φ + (1 φ) exp( λ), y = 0; P {Y = y} = (1 φ) exp(") 2012 10 Chinese Journal of Applied Probability and Statistics Vol.28 No.5 Oct. 2012 (,, 675000) Poisson,,, Gibbs, BIC.,. :,, Gibbs, BIC. : O212.8. 1. (count data), Poisson Poisson., (zeroinflation).,.,,

2012 10 Chinese Journal of Applied Probability and Statistics Vol.28 No.5 Oct. 2012 (,, 675000) Poisson,,, Gibbs, BIC.,. :,, Gibbs, BIC. : O212.8. 1. (count data), Poisson Poisson., (zeroinflation).,.,,

TeSys contactors a.c. coils for 3-pole contactors LC1-D

References a.c. coils for 3-pole contactors LC1-D Control circuit voltage Average resistance Inductance of Reference (1) Weight Uc at 0 C ± 10 % closed circuit For 3-pole " contactors LC1-D09...D38 and

References a.c. coils for 3-pole contactors LC1-D Control circuit voltage Average resistance Inductance of Reference (1) Weight Uc at 0 C ± 10 % closed circuit For 3-pole " contactors LC1-D09...D38 and

ΕΝΑ ΜΑΘΗΜΑΤΙΚΟ ΜΟΝΤΕΛΟ ΕΞΕΛΙΞΗΣ ΕΝΕΡΓΟΥ ΚΑΙ ΣΒΗΣΜΕΝΟΥ ΗΦΑΙΣΤΕΙΟΥ. Γεώργιος Αιµ. Σκιάνης και ηµήτριος Βαϊόπουλος

ΕΝΑ ΜΑΘΗΜΑΤΙΚΟ ΜΟΝΤΕΛΟ ΕΞΕΛΙΞΗΣ ΕΝΕΡΓΟΥ ΚΑΙ ΣΒΗΣΜΕΝΟΥ ΗΦΑΙΣΤΕΙΟΥ Γεώργιος Αιµ. Σκιάνης και ηµήτριος Βαϊόπουλος Πανεπιστήµιο Αθηνών, Τµήµα Γεωλογίας, Εργαστήριο Τηλεανίχνευσης Περίληψη Στην παρούσα εργασία

ΕΝΑ ΜΑΘΗΜΑΤΙΚΟ ΜΟΝΤΕΛΟ ΕΞΕΛΙΞΗΣ ΕΝΕΡΓΟΥ ΚΑΙ ΣΒΗΣΜΕΝΟΥ ΗΦΑΙΣΤΕΙΟΥ Γεώργιος Αιµ. Σκιάνης και ηµήτριος Βαϊόπουλος Πανεπιστήµιο Αθηνών, Τµήµα Γεωλογίας, Εργαστήριο Τηλεανίχνευσης Περίληψη Στην παρούσα εργασία

Math 6 SL Probability Distributions Practice Test Mark Scheme

Math 6 SL Probability Distributions Practice Test Mark Scheme. (a) Note: Award A for vertical line to right of mean, A for shading to right of their vertical line. AA N (b) evidence of recognizing symmetry

Math 6 SL Probability Distributions Practice Test Mark Scheme. (a) Note: Award A for vertical line to right of mean, A for shading to right of their vertical line. AA N (b) evidence of recognizing symmetry

172,,,,. P,. Box (1980)P, Guttman (1967)Rubin (1984)P, Meng (1994), Gelman(1996)De la HorraRodriguez-Bernal (2003). BayarriBerger (2000)P P.. : Casell

P, Guttman (1967)Rubin (1984)P, Meng (1994), Gelman(1996)De la HorraRodriguez-Bernal (2003). BayarriBerger (2000)P P.. : Casell") 20104 Chinese Journal of Applied Probability and Statistics Vol.26 No.2 Apr. 2010 P (,, 200083) P P. Wang (2006)P, P, P,. : P,,,. : O212.1, O212.8. 1., (). : X 1, X 2,, X n N(θ, σ 2 ), σ 2. H 0 : θ = θ

20104 Chinese Journal of Applied Probability and Statistics Vol.26 No.2 Apr. 2010 P (,, 200083) P P. Wang (2006)P, P, P,. : P,,,. : O212.1, O212.8. 1., (). : X 1, X 2,, X n N(θ, σ 2 ), σ 2. H 0 : θ = θ

ΚΑΛΟΓΡΙΔΟΥ ΑΝΑΣΤΑΣΙΑ ΕΝΕΡΓΕΙΑΚΑ ΠΑΡΑΓΩΓΑ ΜΕΤΑΠΤΥΧΙΑΚΗ ΕΡΓΑΣΙΑ ΠΑΝΕΠΙΣΤΗΜΙΟ ΑΙΓΑΙΟΥ ΤΜΗΜΑ ΧΡΗΜΑΤΟΟΙΚΟΝΟΜΙΚΩΝ ΚΑΙ ΑΝΑΛΟΓΙΣΤΙΚΩΝ ΜΑΘΗΜΑΤΙΚΩΝ

ΚΑΛΟΓΡΙΔΟΥ ΑΝΑΣΤΑΣΙΑ ΕΝΕΡΓΕΙΑΚΑ ΠΑΡΑΓΩΓΑ ΜΕΤΑΠΤΥΧΙΑΚΗ ΕΡΓΑΣΙΑ ΠΑΝΕΠΙΣΤΗΜΙΟ ΑΙΓΑΙΟΥ ΤΜΗΜΑ ΧΡΗΜΑΤΟΟΙΚΟΝΟΜΙΚΩΝ ΚΑΙ ΑΝΑΛΟΓΙΣΤΙΚΩΝ ΜΑΘΗΜΑΤΙΚΩΝ Σάμος 14 Φεβρουαρίου 009 ΕΠΙΒΛΕΠΩΝ ΚΑΘΗΓΗΤΗΣ ΚΩΝΣΤΑΝΤΙΝΙΔΗΣ ΔΗΜΗΤΡΙΟΣ

ΚΑΛΟΓΡΙΔΟΥ ΑΝΑΣΤΑΣΙΑ ΕΝΕΡΓΕΙΑΚΑ ΠΑΡΑΓΩΓΑ ΜΕΤΑΠΤΥΧΙΑΚΗ ΕΡΓΑΣΙΑ ΠΑΝΕΠΙΣΤΗΜΙΟ ΑΙΓΑΙΟΥ ΤΜΗΜΑ ΧΡΗΜΑΤΟΟΙΚΟΝΟΜΙΚΩΝ ΚΑΙ ΑΝΑΛΟΓΙΣΤΙΚΩΝ ΜΑΘΗΜΑΤΙΚΩΝ Σάμος 14 Φεβρουαρίου 009 ΕΠΙΒΛΕΠΩΝ ΚΑΘΗΓΗΤΗΣ ΚΩΝΣΤΑΝΤΙΝΙΔΗΣ ΔΗΜΗΤΡΙΟΣ

ΔΘΝΙΚΗ ΥΟΛΗ ΓΗΜΟΙΑ ΓΙΟΙΚΗΗ ΚΑ ΔΚΠΑΙΓΔΤΣΙΚΗ ΔΙΡΑ ΣΔΛΙΚΗ ΔΡΓΑΙΑ

Ε ΔΘΝΙΚΗ ΥΟΛΗ ΓΗΜΟΙΑ ΓΙΟΙΚΗΗ ΚΑ ΔΚΠΑΙΓΔΤΣΙΚΗ ΔΙΡΑ ΣΜΗΜΑ ΓΔΝΙΚΗ ΓΙΟΙΚΗΗ ΣΔΛΙΚΗ ΔΡΓΑΙΑ Θέκα: Η Γηνίθεζε Αιιαγώλ (Change Management) ζην Γεκόζην Σνκέα: Η πεξίπησζε ηεο εθαξκνγήο ηνπ ύγρξνλνπ Γεκνζηνλνκηθνύ

Ε ΔΘΝΙΚΗ ΥΟΛΗ ΓΗΜΟΙΑ ΓΙΟΙΚΗΗ ΚΑ ΔΚΠΑΙΓΔΤΣΙΚΗ ΔΙΡΑ ΣΜΗΜΑ ΓΔΝΙΚΗ ΓΙΟΙΚΗΗ ΣΔΛΙΚΗ ΔΡΓΑΙΑ Θέκα: Η Γηνίθεζε Αιιαγώλ (Change Management) ζην Γεκόζην Σνκέα: Η πεξίπησζε ηεο εθαξκνγήο ηνπ ύγρξνλνπ Γεκνζηνλνκηθνύ

Ó³ Ÿ , º 2(131).. 105Ä ƒ. ± Ï,.. ÊÉ ±μ,.. Šμ ² ±μ,.. Œ Ì ²μ. Ñ Ò É ÉÊÉ Ö ÒÌ ² μ, Ê

.. 105Ä ƒ. ± Ï,.. ÊÉ ±μ,.. Šμ ² ±μ,.. Œ Ì ²μ. Ñ Ò É ÉÊÉ Ö ÒÌ ² μ, Ê") Ó³ Ÿ. 2006.. 3, º 2(131).. 105Ä110 Š 537.311.5; 538.945 Œ ƒ ˆ ƒ Ÿ ˆŠ ˆ ƒ Ÿ ƒ ˆ œ ƒ Œ ƒ ˆ ˆ Š ˆ 4 ². ƒ. ± Ï,.. ÊÉ ±μ,.. Šμ ² ±μ,.. Œ Ì ²μ Ñ Ò É ÉÊÉ Ö ÒÌ ² μ, Ê ³ É É Ö μ ² ³ μ É ³ Í ² Ö Ê³ μ μ ³ É μ μ μ²ö

Ó³ Ÿ. 2006.. 3, º 2(131).. 105Ä110 Š 537.311.5; 538.945 Œ ƒ ˆ ƒ Ÿ ˆŠ ˆ ƒ Ÿ ƒ ˆ œ ƒ Œ ƒ ˆ ˆ Š ˆ 4 ². ƒ. ± Ï,.. ÊÉ ±μ,.. Šμ ² ±μ,.. Œ Ì ²μ Ñ Ò É ÉÊÉ Ö ÒÌ ² μ, Ê ³ É É Ö μ ² ³ μ É ³ Í ² Ö Ê³ μ μ ³ É μ μ μ²ö

- 1+x 2 - x 3 + 7x4. 40 + 127x8. 12 - x5 4 + 31x6. 360 - x 7. - 1+x 2 - x 3 - -

a.bergara@ehu.es - 1 x 2 - - - - - - - Ο - 1x 2 - x 3 - - - - - - 1 x 2 - x 3 7 x4 12-1x 2 - x 3 7x4 12 - x5 4 31x6 360 - x 7 40 127x8 20160 - - - Ο clear; % Coefficients of the equation: a x'b x c

a.bergara@ehu.es - 1 x 2 - - - - - - - Ο - 1x 2 - x 3 - - - - - - 1 x 2 - x 3 7 x4 12-1x 2 - x 3 7x4 12 - x5 4 31x6 360 - x 7 40 127x8 20160 - - - Ο clear; % Coefficients of the equation: a x'b x c

Supplementary Information for

Supplentary Information for Aggregation induced blue-shifted ission molecular picture from QM/MM study Qunyan Wu, a Tian Zhang, a Qian Peng,* b Dong Wang, a and Zhigang Shuai* a a Key Loratory of Organic

Supplentary Information for Aggregation induced blue-shifted ission molecular picture from QM/MM study Qunyan Wu, a Tian Zhang, a Qian Peng,* b Dong Wang, a and Zhigang Shuai* a a Key Loratory of Organic

Development of the Nursing Program for Rehabilitation of Woman Diagnosed with Breast Cancer

Development of the Nursing Program for Rehabilitation of Woman Diagnosed with Breast Cancer Naomi Morota Newman M Key Words woman diagnosed with breast cancer, rehabilitation nursing care program, the

Development of the Nursing Program for Rehabilitation of Woman Diagnosed with Breast Cancer Naomi Morota Newman M Key Words woman diagnosed with breast cancer, rehabilitation nursing care program, the

Quantitative Finance and Investment Core Formula Sheet. Spring 2017

Quaniaive Finance and Invesmen Core Formula Shee Spring 7 Morning and afernoon exam bookles will include a formula package idenical o he one aached o his sudy noe. The exam commiee believe ha by providing

Quaniaive Finance and Invesmen Core Formula Shee Spring 7 Morning and afernoon exam bookles will include a formula package idenical o he one aached o his sudy noe. The exam commiee believe ha by providing

Χρονοσειρές Μάθημα 3

Χρονοσειρές Μάθημα 3 Ασυσχέτιστες (λευκός θόρυβος) και ανεξάρτητες (iid) παρατηρήσεις Chafield C., The Analysis of Time Series, An Inroducion, 6 h ediion,. 38 (Chaer 3): Some auhors refer o make he weaker

Χρονοσειρές Μάθημα 3 Ασυσχέτιστες (λευκός θόρυβος) και ανεξάρτητες (iid) παρατηρήσεις Chafield C., The Analysis of Time Series, An Inroducion, 6 h ediion,. 38 (Chaer 3): Some auhors refer o make he weaker

JMAK の式の一般化と粒子サイズ分布の計算 by T.Koyama

MAK by T.Koyama MAK MAK f () = exp{ fex () = exp (') v(, ') ' () (') ' v (, ') ' f (), (), v (, ') f () () f () () v (, ') f () () v (, ') f () () () = + {exp( A) () f () = exp( K ) () K,,, A *** ***************************************************************************

MAK by T.Koyama MAK MAK f () = exp{ fex () = exp (') v(, ') ' () (') ' v (, ') ' f (), (), v (, ') f () () f () () v (, ') f () () v (, ') f () () () = + {exp( A) () f () = exp( K ) () K,,, A *** ***************************************************************************

Linear singular perturbations of hyperbolic-parabolic type

BULETINUL ACADEMIEI DE ŞTIINŢE A REPUBLICII MOLDOVA. MATEMATICA Number 4, 3, Pages 95 11 ISSN 14 7696 Linear singular perurbaions of hyperbolic-parabolic ype Perjan A. Absrac. We sudy he behavior of soluions

BULETINUL ACADEMIEI DE ŞTIINŢE A REPUBLICII MOLDOVA. MATEMATICA Number 4, 3, Pages 95 11 ISSN 14 7696 Linear singular perurbaions of hyperbolic-parabolic ype Perjan A. Absrac. We sudy he behavior of soluions

is the home less foreign interest rate differential (expressed as it

The model is solved algebraically, excep for a cubic roo which is solved numerically The mehod of soluion is undeermined coefficiens The noaion in his noe corresponds o he noaion in he program The model

The model is solved algebraically, excep for a cubic roo which is solved numerically The mehod of soluion is undeermined coefficiens The noaion in his noe corresponds o he noaion in he program The model

The conditional CAPM does not explain assetpricing. Jonathan Lewellen & Stefan Nagel. HEC School of Management, March 17, 2005

The condiional CAPM does no explain assepricing anomalies Jonahan Lewellen & Sefan Nagel HEC School of Managemen, March 17, 005 Background Size, B/M, and momenum porfolios, 1964 001 Monhly reurns (%) Avg.

The condiional CAPM does no explain assepricing anomalies Jonahan Lewellen & Sefan Nagel HEC School of Managemen, March 17, 005 Background Size, B/M, and momenum porfolios, 1964 001 Monhly reurns (%) Avg.

Experimental Study of Dielectric Properties on Human Lung Tissue

32 2 2013 4 Chinese Journal of Biomedical Engineering Vol. 32 No. 2 April 2013 1 1* 2 1 300072 2 300052 Agilent 4294A 100 Hz ~ 100 MHz Cole-Cole 3 ~ 5 1. 6 ~ 3. 3 R α τ f c P < 0. 05 EIT R318 A 0258-8021

32 2 2013 4 Chinese Journal of Biomedical Engineering Vol. 32 No. 2 April 2013 1 1* 2 1 300072 2 300052 Agilent 4294A 100 Hz ~ 100 MHz Cole-Cole 3 ~ 5 1. 6 ~ 3. 3 R α τ f c P < 0. 05 EIT R318 A 0258-8021

ΑΝΑΛΥΣΗ ΔΙΤΙΜΩΝ ΧΡΟΝΟΣΕΙΡΩΝ: ΒΡΟΧΟΠΤΩΣΕΙΣ ΤΟΥ ΝΟΜΟΥ ΙΩΑΝΝΙΝΩΝ

Ελληνικό Στατιστικό Ινστιτούτο Πρακτικά 8 ου Πανελληνίου Συνεδρίου Στατιστικής (2005) σελ.29-36 ΑΝΑΛΥΣΗ ΔΙΤΙΜΩΝ ΧΡΟΝΟΣΕΙΡΩΝ: ΒΡΟΧΟΠΤΩΣΕΙΣ ΤΟΥ ΝΟΜΟΥ ΙΩΑΝΝΙΝΩΝ Μανώλης Δρυμώνης και Μαρία Κατέρη Τμήμα Στατιστικής

Ελληνικό Στατιστικό Ινστιτούτο Πρακτικά 8 ου Πανελληνίου Συνεδρίου Στατιστικής (2005) σελ.29-36 ΑΝΑΛΥΣΗ ΔΙΤΙΜΩΝ ΧΡΟΝΟΣΕΙΡΩΝ: ΒΡΟΧΟΠΤΩΣΕΙΣ ΤΟΥ ΝΟΜΟΥ ΙΩΑΝΝΙΝΩΝ Μανώλης Δρυμώνης και Μαρία Κατέρη Τμήμα Στατιστικής

Retrieval of Seismic Data Recorded on Open-reel-type Magnetic Tapes (MT) by Using Existing Devices

by Using Existing Devices") No. 3 + 1,**- Technical Research Report, Earthquake Research Institute, University of Tokyo, No. 3, pp. + 1,,**-. MT * ** *** Retrieval of Seismic Data Recorded on Open-reel-type Magnetic Tapes (MT) by

No. 3 + 1,**- Technical Research Report, Earthquake Research Institute, University of Tokyo, No. 3, pp. + 1,,**-. MT * ** *** Retrieval of Seismic Data Recorded on Open-reel-type Magnetic Tapes (MT) by

Polyvinyl Chloride PVC, The effects of organotin thermal stabilizers on the dehydrochlorination of TPUΠPVC blends

No. 4 J ul.,2004 Polyvinyl Chloride 4 2004 7 TPUΠPVC Ξ,, (, 210009) [ ] [ ] Π,, :,, 395A T - 137 DB TL CaSt 2, [ ] TQ325. 3 TQ328. 3 [ ] A [ ] 1009-7937 (2004) 04-0028 - 06 The effects of organotin thermal

No. 4 J ul.,2004 Polyvinyl Chloride 4 2004 7 TPUΠPVC Ξ,, (, 210009) [ ] [ ] Π,, :,, 395A T - 137 DB TL CaSt 2, [ ] TQ325. 3 TQ328. 3 [ ] A [ ] 1009-7937 (2004) 04-0028 - 06 The effects of organotin thermal

ΧΩΡΙΚΑ ΟΙΚΟΝΟΜΕΤΡΙΚΑ ΥΠΟΔΕΙΓΜΑΤΑ ΣΤΗΝ ΕΚΤΙΜΗΣΗ ΤΩΝ ΤΙΜΩΝ ΤΩΝ ΑΚΙΝΗΤΩΝ SPATIAL ECONOMETRIC MODELS FOR VALUATION OF THE PROPERTY PRICES

1 ο Συνέδριο Χωρικής Ανάλυσης: Πρακτικά, Αθήνα, 013, Σ. Καλογήρου (Επ.) ISBN: 978-960-86818-6-6 ΧΩΡΙΚΑ ΟΙΚΟΝΟΜΕΤΡΙΚΑ ΥΠΟΔΕΙΓΜΑΤΑ ΣΤΗΝ ΕΚΤΙΜΗΣΗ ΤΩΝ ΤΙΜΩΝ ΤΩΝ ΑΚΙΝΗΤΩΝ Μαριάνθη Στάμου 1*, Άγγελος Μιμής και

1 ο Συνέδριο Χωρικής Ανάλυσης: Πρακτικά, Αθήνα, 013, Σ. Καλογήρου (Επ.) ISBN: 978-960-86818-6-6 ΧΩΡΙΚΑ ΟΙΚΟΝΟΜΕΤΡΙΚΑ ΥΠΟΔΕΙΓΜΑΤΑ ΣΤΗΝ ΕΚΤΙΜΗΣΗ ΤΩΝ ΤΙΜΩΝ ΤΩΝ ΑΚΙΝΗΤΩΝ Μαριάνθη Στάμου 1*, Άγγελος Μιμής και

7 Η ΕΞΕΡΓΕΙΑ. 7.1 Εισαγωγή και ορισμός της έννοιας της εξέργειας. 7.2 Ενέργεια, ύλη και ποιότητα

7 Η ΕΞΕΡΓΕΙΑ 7.1 Εισαγωγή και ορισμός της έννοιας της εξέργειας Όπου υπάρχει υπολογισμός ενεργειακών μεγεθών, υπάρχει παράλληλα μεγάλη σύγχυση στα μεγέθη που πρέπει να μετρηθούν και να εκτιμηθούν. Πολύ

7 Η ΕΞΕΡΓΕΙΑ 7.1 Εισαγωγή και ορισμός της έννοιας της εξέργειας Όπου υπάρχει υπολογισμός ενεργειακών μεγεθών, υπάρχει παράλληλα μεγάλη σύγχυση στα μεγέθη που πρέπει να μετρηθούν και να εκτιμηθούν. Πολύ

ΑΝΑΛΥΣΗ ΚΑΙ ΠΡΟΒΛΕΨΗ ΤΟΥ ΣΥΝΟΛΙΚΟΥ ΑΡΙΘΜΟΥ ΤΩΝ ΓΕΩΡΓΙΚΩΝ ΕΛΚΥΣΤΗΡΩΝ ΤΗΣ ΕΛΛΑΔΑΣ ΜΕ ΣΥΝΑΡΤΗΣΕΙΣ ΧΡΟΝΙΚΗΣ ΤΑΣΗΣ

Ελληνικό Στατιστικό Ινστιτούτο Πρακτικά 8 ου Πανελληνίου Συνεδρίου Στατιστικής (2005) σελ.409-46 ΑΝΑΛΥΣΗ ΚΑΙ ΠΡΟΒΛΕΨΗ ΤΟΥ ΣΥΝΟΛΙΚΟΥ ΑΡΙΘΜΟΥ ΤΩΝ ΓΕΩΡΓΙΚΩΝ ΕΛΚΥΣΤΗΡΩΝ ΤΗΣ ΕΛΛΑΔΑΣ ΜΕ ΣΥΝΑΡΤΗΣΕΙΣ ΧΡΟΝΙΚΗΣ

Ελληνικό Στατιστικό Ινστιτούτο Πρακτικά 8 ου Πανελληνίου Συνεδρίου Στατιστικής (2005) σελ.409-46 ΑΝΑΛΥΣΗ ΚΑΙ ΠΡΟΒΛΕΨΗ ΤΟΥ ΣΥΝΟΛΙΚΟΥ ΑΡΙΘΜΟΥ ΤΩΝ ΓΕΩΡΓΙΚΩΝ ΕΛΚΥΣΤΗΡΩΝ ΤΗΣ ΕΛΛΑΔΑΣ ΜΕ ΣΥΝΑΡΤΗΣΕΙΣ ΧΡΟΝΙΚΗΣ

2 ~ 8 Hz Hz. Blondet 1 Trombetti 2-4 Symans 5. = - M p. M p. s 2 x p. s 2 x t x t. + C p. sx p. + K p. x p. C p. s 2. x tp x t.

36 2010 8 8 Vol 36 No 8 JOURNAL OF BEIJING UNIVERSITY OF TECHNOLOGY Aug 2010 Ⅰ 100124 TB 534 + 2TP 273 A 0254-0037201008 - 1091-08 20 Hz 2 ~ 8 Hz 1988 Blondet 1 Trombetti 2-4 Symans 5 2 2 1 1 1b 6 M p

36 2010 8 8 Vol 36 No 8 JOURNAL OF BEIJING UNIVERSITY OF TECHNOLOGY Aug 2010 Ⅰ 100124 TB 534 + 2TP 273 A 0254-0037201008 - 1091-08 20 Hz 2 ~ 8 Hz 1988 Blondet 1 Trombetti 2-4 Symans 5 2 2 1 1 1b 6 M p