9.1 Introduction 9.2 Lags in the Error Term: Autocorrelation 9.3 Estimating an AR(1) Error Model 9.4 Testing for Autocorrelation 9.

|

|

|

- Ἑλένη Παπαϊωάννου

- 6 χρόνια πριν

- Προβολές:

Transcript

1

Error Model 9.")

2 9.1 Inroducion 9.2 Lags in he Error Term: Auocorrelaion 9.3 Esimaing an AR(1) Error Model 9.4 Tesing for Auocorrelaion 9.5 An Inroducion o Forecasing: Auoregressive Models 9.6 Finie Disribued Lags 9.7 Auoregressive Disribued Lag Models

3 Figure 9.1

4 y = f( x, x, x,...) 1 2 y = f( y, x ) 1 y = f( x) + e e = f ( e 1)

Time Series of a")

5 Figure 9.2(a) Time Series of a Saionary Variable

6 Figure 9.2(b) Time Series of a Nonsaionary Variable ha is Slow Turning or Wandering

7 Figure 9.2(c) Time Series of a Nonsaionary Variable ha Trends

=β +β ln (")

8 9.2.1 Area Response Model for Sugar Cane ln ln ( A) =β +β ln ( P) 1 2 ( ) ln ( ) A = β+β P + e 1 2 y = β+β x + e 1 2 e = ρ e + v 1

9 y = β+β x + e 1 2 e = ρ e + v 1 Ev = v =σ v v = s 2 ( ) 0 var( ) v cov(, s) 0 for 1<ρ< 1

10 Ee ( ) = 0 var( ) 2 σv =σ = 1 ρ 2 e e 2 2 ( e e ) k cov, = σρ k > 0 k e

11 corr( e, e ) k cov( e, e ) cov( e, e ) σρ = = = =ρ var( e ) var 2 k k k e 2 ( e ) var( e) σ k e k corr( e, e 1) = ρ yˆ = x (se) (.061) (.277)

12

13 Figure 9.3 Leas Squares Residuals Ploed Agains Time

14 r xy ( x x)( y y) cov( x, y) = 1 = = var( x)var( y) ( x x) ( y y) T T T 2 2 = 1 = 1 r 1 cov( e, e ) = = var( e ) T 1 = 2 T = 2 ee 垐 eˆ 1 2 1

15 The exisence of AR(1) errors implies: The leas squares esimaor is sill a linear and unbiased esimaor, bu i is no longer bes. There is anoher esimaor wih a smaller variance. The sandard errors usually compued for he leas squares esimaor are incorrec. Confidence inervals and hypohesis ess ha use hese sandard errors may be misleading.

16 Sugar cane example The wo ses of sandard errors, along wih he esimaed equaion are: yˆ = x (.061) (.277) 'incorrec' se's (.062) (.378) 'correc' se's The 95% confidence inervals for β 2 are: (.211, 1.340) (incorrec) (.006,1.546) (correc)

17 y = β+β x + e 1 2 e = ρ e + v 1 y = β+β x +ρ e + v e = y β β x

18 ρ e =ρy ρβ ρβ x y =β (1 ρ ) +β x +ρy ρβ x + v ln( A ) = ln( P) e =.422e + v 1 (se) (.092) (.259) (.166)

19 I can be shown ha nonlinear leas squares esimaion of (9.24) is equivalen o using an ieraive generalized leas squares esimaor called he Cochrane-Orcu procedure. Deails are provided in Appendix 9A.

20 y =β (1 ρ ) +β x ρβ x +ρ y + v y = δ+δ x +δ x +θ y + v δ =β1(1 ρ) δ 0 =β2 δ 1 = ρβ2 θ 1 =ρ yˆ = x.611 x +.404y 1 1 (se) (.656) (.280) (.297) (.167)

21 9.4.1 Residual Correlogram H : ρ = 0 H : ρ z = Tr1 N(0,1) z = =

22 9.4.1 Residual Correlogram r or r T T 1 1 r k or rk T T cov( e, e ) E( ee ) ρ = = k k k 2 var( e) E( e )

23 Figure 9.4 Correlogram for Leas Squares Residuals from Sugar Cane Example

24 y = β+β x + e 1 2 y = β (1 ρ ) +β x +ρy ρβ x + v

25 Figure 9.5 Correlogram for Nonlinear Leas Squares Residuals from Sugar Cane Example

26 y = β+β x +ρ e + v = F = p-value =.021 y = β+β x +ρ e垐 + v b + b x + e垐 =β +β x +ρ e + v?

27 e垐 = ( β b) + ( β b ) x +ρ e + v? =γ +γ x +ρ e垐 + v LM T R 2 = = =

28 y =δ+θ y +θ y + L+θ y + v p p CPI CPI 1 y = ( ln( CPI) ln( CPI 1) ) CPI 1 INFLN = INFLN.2179 INFLN INFLN (se) (.0253) (.0615) (.0645) (.0613)

29 Figure 9.6 Correlogram for Leas Squares Residuals from AR(3) Model for Inflaion

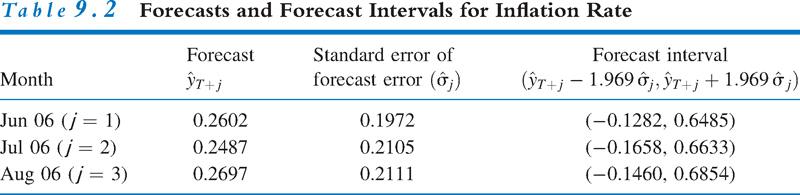

30 y =δ+θ y +θ y +θ y + v y = δ+θ y +θ y +θ y + v T+ 1 1 T 2 T 1 3 T 2 T+ 1 yˆ =δ+θ 垐 y +θ 垐 y +θ y T+ 1 1 T 2 T 1 3 T 2 = =.2602

+ ( θ θ ) y + ( θ θ 垐 ) y + ( θ θ ) y + v 1 T+ 1 T+ 1 1 1 T 2 2 T 1 3 3")

31 y垐 =δ+θ 垐 y +θ 垐 y +θ y T+ 2 1 T+ 1 2 T 3 T 1 = =.2487 u = y yˆ = ( δ δ 垐 ) + ( θ θ ) y + ( θ θ 垐 ) y + ( θ θ ) y + v 1 T+ 1 T T 2 2 T T 2 T+ 1

32

33 u = v + 1 T 1 u = θ ( y yˆ ) + v =θ u + v =θ v + v 2 1 T+ 1 T+ 1 T T+ 2 1 T+ 1 T+ 2 u =θ u +θ u + v = ( θ +θ ) v +θ v + v T T+ 1 1 T+ 2 T+ 3

34 σ = var( u ) =σ v σ = var( u ) =σ (1 +θ ) v 1 σ = var( u ) =σ [( θ +θ ) +θ + 1] v ( y垐 1.96 σ, y垐 σ ) T + j j T + j j

35 y = α+β 0x +β 1x 1+β 2x 2 + L+β qx q + v, = q+ 1, K, T E( y ) x s = β s WAGE WAGE 1 x = ( ln( WAGE) ln( WAGE 1) ) WAGE 1

36

37

38 y = δ+δ x +δ x + L+δ x +θ y + L+θ y + v q q 1 1 p p y =α+β x +β x +β x +β x + L+ e =α+ β x + e s= 0 s s

39 Figure 9.7 Correlogram for Leas Squares Residuals from Finie Disribued Lag Model

40 INFLN = PCWAGE PCWAGE PCWAGE 1 2 (se) (.0288) (.0761) (.0812) (.0812) PCWAGE INFLN.1976 INFLN (.0829) (.0604) (.0604)

41 Figure 9.8 Correlogram for Leas Squares Residuals from Auoregressive Disribued Lag Model

42 y = δ+δ x +δ x +δ x +δ x +θ y +θ y + v β 垐 =δ = β 垐 =θβ 垐 +δ = = β 垐 =θβ 垐 +θ β 垐 +δ = β 垐 =θβ 垐 +θ β 垐 +δ = β 垐 =θβ 垐 +θ β? =

43 Figure 9.9 Disribued Lag Weighs for Auoregressive Disribued Lag Model

44 Principles of Economerics, 3rd Ediion Slide 9-44

45 Principles of Economerics, 3rd Ediion Slide 9-45

46 y = β+β x + e e =ρ e + v y =β +β x +ρy ρβ ρβ x + v (9A.1) ( 1 ) ( ) y ρ y =β ρ +β x ρ x + v (9A.2) y = y ρ y x = x ρ x x = ρ Principles of Economerics, 3rd Ediion Slide 9-46

47 y = x β+ x β+ v (9A.3) y β β x =ρ( y β β x ) + v (9A.4) Principles of Economerics, 3rd Ediion Slide 9-47

48 y1 = β+ 1 x1β+ 2 e1 1 ρ y = 1 ρ β + 1 ρ xβ + 1 ρ e y = x β+ x β+ e (9A.5) Principles of Economerics, 3rd Ediion y = 1 ρ y x = 1 ρ x = 1 ρ x e = 1 ρ e (9A.6) Slide 9-48

49 σv var( e ) (1 ) var( ) (1 ) 1 ρ = ρ e1 = ρ =σ 2 v Principles of Economerics, 3rd Ediion Slide 9-49

50 H : ρ = 0 H : ρ> d = T ( e垐 ) 2 e 1 = 2 T = 1 eˆ 2 (9B.1) Principles of Economerics, 3rd Ediion Slide 9-50

51 d = T T T 2 2 e垐垐 + e 1 2 ee 1 = 2 = 2 = 2 T 2 eˆ = 1 T T T 2 2 e垐 垐 e 1 ee 1 = 2 = 2 = 2 2 T T T e垐? e e = 1 = 1 = 1 = + (9B.2) r 1 Principles of Economerics, 3rd Ediion Slide 9-51

52 d 21 r ( ) 1 (9B.3) d d c Principles of Economerics, 3rd Ediion Slide 9-52

53 Figure 9A.1: Principles of Economerics, 3rd Ediion Slide 9-53

54 Figure 9A.2: Principles of Economerics, 3rd Ediion Slide 9-54

55 The Durbin-Wason bounds es. if d < d, rejec H : ρ= 0 and accep H : ρ> 0; Lc 0 1 if d > d, do no rejec H : ρ= 0; Uc if d < d < d he es is inconclusive. Lc Uc, 0 Principles of Economerics, 3rd Ediion Slide 9-55

56 y =α+β x +β x +β x +β x + L+ e =α+ β x + e s s s= 0 y = δ+δ x +δ x + L+δ x +θ y + L+θ y + v q q 1 1 p p Principles of Economerics, 3rd Ediion Slide 9-56

y = δ+δ x +θ y 1 0 1 1 2 (9C.")

57 y = δ+δ x +θ y + v (9C.1) y = δ+δ x +θ y (9C.2) y = δ+δ x +θ y =δ+δ x +θ ( δ+δ x +θ y ) =δ+θδ+δ x +θδ x +θ y Principles of Economerics, 3rd Ediion Slide 9-57

58 y =δ+θδ+δ x +θδ x +θ ( δ+δ x +θ y ) =δ+θδ+θ δ+δ x +θδ x +θ δ x +θ y y =δ+θδ+θ δ+ L+θ δ 2 j δ x +θδ x +θ δ x + L+θ δ x +θ y 2 j j j 1 ( j+ 1) (9C.3) j 2 j s j L 1 0 1x s 1 y ( j+ 1) s= 0 =δ (1 +θ +θ + +θ ) + δ θ +θ Principles of Economerics, 3rd Ediion Slide 9-58

59 y =α+ s= 0 δ θ s 0 1 x s (9C.4) α=δ 2 (1 +θ +θ L) = 1 θ 1 δ y = α+ β x + e s s s= 0 Principles of Economerics, 3rd Ediion Slide 9-59

60 β =δ θ s s 0 1 δ β =δ +θ +θ + = θ 2 0 s 0(1 1 1 L) s= Principles of Economerics, 3rd Ediion Slide 9-60

61 y = δ+δ x +δ x +δ x +δ x +θ y +θ y +v (9C.5) β =δ 0 0 β =θβ +δ β =θβ +θ β +δ β =θβ +θ β +δ β =θβ +θ β M β =θβ 1 1+θ2β 2 for 4 s s s s (9C.6) Principles of Economerics, 3rd Ediion Slide 9-61

62 ˆ y + y + y 3 T T 1 T 2 yt + 1 = yˆ =α y +α(1 α ) y +α(1 α ) y +L 1 2 T+ 1 T T 1 T 2 (9D.1) (1 α ) yˆ =α(1 α ) y +α(1 α ) y +α(1 α ) y T T 1 T 2 T 3 (9D.2) y垐 = α y + + (1 α ) y T 1 T T Principles of Economerics, 3rd Ediion Slide 9-62

63 Figure 9A.3: Exponenial Smoohing Forecass for wo alernaive values of α Principles of Economerics, 3rd Ediion Slide 9-63

Χρονοσειρές Μάθημα 3

Χρονοσειρές Μάθημα 3 Ασυσχέτιστες (λευκός θόρυβος) και ανεξάρτητες (iid) παρατηρήσεις Chafield C., The Analysis of Time Series, An Inroducion, 6 h ediion,. 38 (Chaer 3): Some auhors refer o make he weaker

Χρονοσειρές Μάθημα 3 Ασυσχέτιστες (λευκός θόρυβος) και ανεξάρτητες (iid) παρατηρήσεις Chafield C., The Analysis of Time Series, An Inroducion, 6 h ediion,. 38 (Chaer 3): Some auhors refer o make he weaker

8.1 The Nature of Heteroskedasticity 8.2 Using the Least Squares Estimator 8.3 The Generalized Least Squares Estimator 8.

8.1 The Nature of Heteroskedastcty 8. Usng the Least Squares Estmator 8.3 The Generalzed Least Squares Estmator 8.4 Detectng Heteroskedastcty E( y) = β+β 1 x e = y E( y ) = y β β x 1 y = β+β x + e 1 Fgure

8.1 The Nature of Heteroskedastcty 8. Usng the Least Squares Estmator 8.3 The Generalzed Least Squares Estmator 8.4 Detectng Heteroskedastcty E( y) = β+β 1 x e = y E( y ) = y β β x 1 y = β+β x + e 1 Fgure

( ) ( t) ( 0) ( ) dw w. = = β. Then the solution of (1.1) is easily found to. wt = t+ t. We generalize this to the following nonlinear differential

( t) ( 0) ( ) dw w. = = β. Then the solution of (1.1) is easily found to. wt = t+ t. We generalize this to the following nonlinear differential") Periodic oluion of van der Pol differenial equaion. by A. Arimoo Deparmen of Mahemaic Muahi Iniue of Technology Tokyo Japan in Seminar a Kiami Iniue of Technology January 8 9. Inroducion Le u conider a

Periodic oluion of van der Pol differenial equaion. by A. Arimoo Deparmen of Mahemaic Muahi Iniue of Technology Tokyo Japan in Seminar a Kiami Iniue of Technology January 8 9. Inroducion Le u conider a

Supplementary Appendix

Supplementary Appendix Measuring crisis risk using conditional copulas: An empirical analysis of the 2008 shipping crisis Sebastian Opitz, Henry Seidel and Alexander Szimayer Model specification Table

Supplementary Appendix Measuring crisis risk using conditional copulas: An empirical analysis of the 2008 shipping crisis Sebastian Opitz, Henry Seidel and Alexander Szimayer Model specification Table

HW 3 Solutions 1. a) I use the auto.arima R function to search over models using AIC and decide on an ARMA(3,1)

I use the auto.arima R function to search over models using AIC and decide on an ARMA(3,1)") HW 3 Solutions a) I use the autoarima R function to search over models using AIC and decide on an ARMA3,) b) I compare the ARMA3,) to ARMA,0) ARMA3,) does better in all three criteria c) The plot of the

HW 3 Solutions a) I use the autoarima R function to search over models using AIC and decide on an ARMA3,) b) I compare the ARMA3,) to ARMA,0) ARMA3,) does better in all three criteria c) The plot of the

d dt S = (t)si d dt R = (t)i d dt I = (t)si (t)i

si d dt R = (t)i d dt I = (t)si (t)i") d d S = ()SI d d I = ()SI ()I d d R = ()I d d S = ()SI μs + fi + hr d d I = + ()SI (μ + + f + ())I d d R = ()I (μ + h)r d d P(S,I,) = ()(S +1)(I 1)P(S +1, I 1, ) +()(I +1)P(S,I +1, ) (()SI + ()I)P(S,I,)

d d S = ()SI d d I = ()SI ()I d d R = ()I d d S = ()SI μs + fi + hr d d I = + ()SI (μ + + f + ())I d d R = ()I (μ + h)r d d P(S,I,) = ()(S +1)(I 1)P(S +1, I 1, ) +()(I +1)P(S,I +1, ) (()SI + ()I)P(S,I,)

Introduction to the ML Estimation of ARMA processes

Introduction to the ML Estimation of ARMA processes Eduardo Rossi University of Pavia October 2013 Rossi ARMA Estimation Financial Econometrics - 2013 1 / 1 We consider the AR(p) model: Y t = c + φ 1 Y

Introduction to the ML Estimation of ARMA processes Eduardo Rossi University of Pavia October 2013 Rossi ARMA Estimation Financial Econometrics - 2013 1 / 1 We consider the AR(p) model: Y t = c + φ 1 Y

ΚΕΦΑΛΑΙΟ 2 ΟΙΚΟΝΟΜΕΤΡΙΚΑ ΥΠΟΔΕΙΓΜΑΤΑ ΧΡΟΝΙΚΩΝ ΣΕΙΡΩΝ. 2.1 Σύντομη ανασκόπηση του κλασσικού υποδείγματος

ΚΕΦΑΛΑΙΟ ΟΙΚΟΝΟΜΕΤΡΙΚΑ ΥΠΟΔΕΙΓΜΑΤΑ ΧΡΟΝΙΚΩΝ ΣΕΙΡΩΝ.1 Σύντομη ανασκόπηση του κλασσικού υποδείγματος παλινδρόμησης συνήθων ελαχίστων τετραγώνων (Ordinary Leas Squares regression model).. Ένα παράδειγμα οικονομετρικού

ΚΕΦΑΛΑΙΟ ΟΙΚΟΝΟΜΕΤΡΙΚΑ ΥΠΟΔΕΙΓΜΑΤΑ ΧΡΟΝΙΚΩΝ ΣΕΙΡΩΝ.1 Σύντομη ανασκόπηση του κλασσικού υποδείγματος παλινδρόμησης συνήθων ελαχίστων τετραγώνων (Ordinary Leas Squares regression model).. Ένα παράδειγμα οικονομετρικού

Levin Lin(1992) Oh(1996),Wu(1996) Papell(1997) Im, Pesaran Shin(1996) Canzoneri, Cumby Diba(1999) Lee, Pesaran Smith(1997) FGLS SUR

Oh(1996),Wu(1996) Papell(1997) Im, Pesaran Shin(1996) Canzoneri, Cumby Diba(1999) Lee, Pesaran Smith(1997) FGLS SUR") EVA M, SWEEEY R 3,. ;. McDonough ; 3., 3006 ; ; F4.0 A Levin Lin(99) Im, Pesaran Shin(996) Levin Lin(99) Oh(996),Wu(996) Paell(997) Im, Pesaran Shin(996) Canzoner Cumby Diba(999) Levin Lin(99) Coe Helman(995)

EVA M, SWEEEY R 3,. ;. McDonough ; 3., 3006 ; ; F4.0 A Levin Lin(99) Im, Pesaran Shin(996) Levin Lin(99) Oh(996),Wu(996) Paell(997) Im, Pesaran Shin(996) Canzoner Cumby Diba(999) Levin Lin(99) Coe Helman(995)

4.6 Autoregressive Moving Average Model ARMA(1,1)

") 84 CHAPTER 4. STATIONARY TS MODELS 4.6 Autoregressive Moving Average Model ARMA(,) This section is an introduction to a wide class of models ARMA(p,q) which we will consider in more detail later in this

84 CHAPTER 4. STATIONARY TS MODELS 4.6 Autoregressive Moving Average Model ARMA(,) This section is an introduction to a wide class of models ARMA(p,q) which we will consider in more detail later in this

Appendix. The solution begins with Eq. (2.15) from the text, which we repeat here for 1, (A.1)

from the text, which we repeat here for 1, (A.1)") Aenix Aenix A: The equaion o he sock rice. The soluion egins wih Eq..5 rom he ex, which we reea here or convenience as Eq.A.: [ [ E E X, A. c α where X u ε, α γ, an c α y AR. Take execaions o Eq. A. as

Aenix Aenix A: The equaion o he sock rice. The soluion egins wih Eq..5 rom he ex, which we reea here or convenience as Eq.A.: [ [ E E X, A. c α where X u ε, α γ, an c α y AR. Take execaions o Eq. A. as

The Student s t and F Distributions Page 1

The Suden s and F Disribuions Page The Fundamenal Transformaion formula for wo random variables: Consider wo random variables wih join probabiliy disribuion funcion f (, ) simulaneously ake on values in

The Suden s and F Disribuions Page The Fundamenal Transformaion formula for wo random variables: Consider wo random variables wih join probabiliy disribuion funcion f (, ) simulaneously ake on values in

Time Series Analysis Final Examination

Dr. Sevap Kesel Time Series Aalysis Fial Examiaio Quesio ( pois): Assume you have a sample of ime series wih observaios yields followig values for sample auocorrelaio Lag (m) ˆ( ρ m) -0. 0.09 0. Par a.

Dr. Sevap Kesel Time Series Aalysis Fial Examiaio Quesio ( pois): Assume you have a sample of ime series wih observaios yields followig values for sample auocorrelaio Lag (m) ˆ( ρ m) -0. 0.09 0. Par a.

Statistics 104: Quantitative Methods for Economics Formula and Theorem Review

Harvard College Statistics 104: Quantitative Methods for Economics Formula and Theorem Review Tommy MacWilliam, 13 tmacwilliam@college.harvard.edu March 10, 2011 Contents 1 Introduction to Data 5 1.1 Sample

Harvard College Statistics 104: Quantitative Methods for Economics Formula and Theorem Review Tommy MacWilliam, 13 tmacwilliam@college.harvard.edu March 10, 2011 Contents 1 Introduction to Data 5 1.1 Sample

Α. Μπατσίδης Πρόχειρες βοηθητικές διδακτικές σημειώσεις

Α. Μπατσίδης Πρόχειρες βοηθητικές διδακτικές σημειώσεις Οι παρούσες σημειώσεις επιχειρούν να αποτελέσουν μια βοήθεια τόσο στην παρακολούθηση της διάλεξης όσο και στη μελέτη κάποιων εκ των θεμάτων της Γραμμικής

Α. Μπατσίδης Πρόχειρες βοηθητικές διδακτικές σημειώσεις Οι παρούσες σημειώσεις επιχειρούν να αποτελέσουν μια βοήθεια τόσο στην παρακολούθηση της διάλεξης όσο και στη μελέτη κάποιων εκ των θεμάτων της Γραμμικής

Ηλεκτρονικοί Υπολογιστές IV

ΠΑΝΕΠΙΣΤΗΜΙΟ ΙΩΑΝΝΙΝΩΝ ΑΝΟΙΚΤΑ ΑΚΑΔΗΜΑΪΚΑ ΜΑΘΗΜΑΤΑ Ηλεκτρονικοί Υπολογιστές IV Μοντέλα χρονολογικών σειρών Διδάσκων: Επίκουρος Καθηγητής Αθανάσιος Σταυρακούδης Άδειες Χρήσης Το παρόν εκπαιδευτικό υλικό

ΠΑΝΕΠΙΣΤΗΜΙΟ ΙΩΑΝΝΙΝΩΝ ΑΝΟΙΚΤΑ ΑΚΑΔΗΜΑΪΚΑ ΜΑΘΗΜΑΤΑ Ηλεκτρονικοί Υπολογιστές IV Μοντέλα χρονολογικών σειρών Διδάσκων: Επίκουρος Καθηγητής Αθανάσιος Σταυρακούδης Άδειες Χρήσης Το παρόν εκπαιδευτικό υλικό

FORMULAS FOR STATISTICS 1

FORMULAS FOR STATISTICS 1 X = 1 n Sample statistics X i or x = 1 n x i (sample mean) S 2 = 1 n 1 s 2 = 1 n 1 (X i X) 2 = 1 n 1 (x i x) 2 = 1 n 1 Xi 2 n n 1 X 2 x 2 i n n 1 x 2 or (sample variance) E(X)

FORMULAS FOR STATISTICS 1 X = 1 n Sample statistics X i or x = 1 n x i (sample mean) S 2 = 1 n 1 s 2 = 1 n 1 (X i X) 2 = 1 n 1 (x i x) 2 = 1 n 1 Xi 2 n n 1 X 2 x 2 i n n 1 x 2 or (sample variance) E(X)

Mean-Variance Analysis

Mean-Variance Analysis Jan Schneider McCombs School of Business University of Texas at Austin Jan Schneider Mean-Variance Analysis Beta Representation of the Risk Premium risk premium E t [Rt t+τ ] R1

Mean-Variance Analysis Jan Schneider McCombs School of Business University of Texas at Austin Jan Schneider Mean-Variance Analysis Beta Representation of the Risk Premium risk premium E t [Rt t+τ ] R1

Μάθημα 5-6: Στάσιμες πολυμεταβλητές χρονοσειρές και μοντέλα Διασυσχέτιση Διανυσματικά αυτοπαλίνδρομα μοντέλα Δίκτυα από πολυμεταβλητές χρονοσειρές

Μάθημα 5-6: Στάσιμες πολυμεταβλητές χρονοσειρές και μοντέλα Διασυσχέτιση Διανυσματικά αυτοπαλίνδρομα μοντέλα Δίκτυα από πολυμεταβλητές χρονοσειρές Αιτιότητα κατά Granger Ασκήσεις Ανάλυση μονομεταβλητής

Μάθημα 5-6: Στάσιμες πολυμεταβλητές χρονοσειρές και μοντέλα Διασυσχέτιση Διανυσματικά αυτοπαλίνδρομα μοντέλα Δίκτυα από πολυμεταβλητές χρονοσειρές Αιτιότητα κατά Granger Ασκήσεις Ανάλυση μονομεταβλητής

The random walk model with autoregressive errors

MPRA Munich Personal RePEc Archive The random walk model wih auoregressive errors Halkos George and Kevork Ilias Universiy of Thessaly, Deparmen of Economics 2005 Online a hp://mpra.ub.uni-muenchen.de/33312/

MPRA Munich Personal RePEc Archive The random walk model wih auoregressive errors Halkos George and Kevork Ilias Universiy of Thessaly, Deparmen of Economics 2005 Online a hp://mpra.ub.uni-muenchen.de/33312/

EE101: Resonance in RLC circuits

EE11: Resonance in RLC circuits M. B. Patil mbatil@ee.iitb.ac.in www.ee.iitb.ac.in/~sequel Deartment of Electrical Engineering Indian Institute of Technology Bombay I V R V L V C I = I m = R + jωl + 1/jωC

EE11: Resonance in RLC circuits M. B. Patil mbatil@ee.iitb.ac.in www.ee.iitb.ac.in/~sequel Deartment of Electrical Engineering Indian Institute of Technology Bombay I V R V L V C I = I m = R + jωl + 1/jωC

Tự tương quan (Autocorrelation)

") Tự ương quan (Auocorrelaion) Đinh Công Khải Tháng 04/2016 1 Nội dung 1. Tự ương quan là gì? 2. Hậu quả của việc ước lượng bỏ qua ự ương quan? 3. Làm sao để phá hiện ự ương quan? 4. Các biện pháp khắc phục?

Tự ương quan (Auocorrelaion) Đinh Công Khải Tháng 04/2016 1 Nội dung 1. Tự ương quan là gì? 2. Hậu quả của việc ước lượng bỏ qua ự ương quan? 3. Làm sao để phá hiện ự ương quan? 4. Các biện pháp khắc phục?

6.3 Forecasting ARMA processes

122 CHAPTER 6. ARMA MODELS 6.3 Forecasting ARMA processes The purpose of forecasting is to predict future values of a TS based on the data collected to the present. In this section we will discuss a linear

122 CHAPTER 6. ARMA MODELS 6.3 Forecasting ARMA processes The purpose of forecasting is to predict future values of a TS based on the data collected to the present. In this section we will discuss a linear

Tự tương quan (Autoregression)

") Tự ương quan (Auoregression) Đinh Công Khải Tháng 05/013 1 Nội dung 1. Tự ương quan (AR) là gì?. Hậu quả của việc ước lượng bỏ qua AR? 3. Làm sao để phá hiện AR? 4. Các biện pháp khắc phục? 1 Tự ương quan

Tự ương quan (Auoregression) Đinh Công Khải Tháng 05/013 1 Nội dung 1. Tự ương quan (AR) là gì?. Hậu quả của việc ước lượng bỏ qua AR? 3. Làm sao để phá hiện AR? 4. Các biện pháp khắc phục? 1 Tự ương quan

CHAPTER 25 SOLVING EQUATIONS BY ITERATIVE METHODS

CHAPTER 5 SOLVING EQUATIONS BY ITERATIVE METHODS EXERCISE 104 Page 8 1. Find the positive root of the equation x + 3x 5 = 0, correct to 3 significant figures, using the method of bisection. Let f(x) =

CHAPTER 5 SOLVING EQUATIONS BY ITERATIVE METHODS EXERCISE 104 Page 8 1. Find the positive root of the equation x + 3x 5 = 0, correct to 3 significant figures, using the method of bisection. Let f(x) =

Module 5. February 14, h 0min

Module 5 Stationary Time Series Models Part 2 AR and ARMA Models and Their Properties Class notes for Statistics 451: Applied Time Series Iowa State University Copyright 2015 W. Q. Meeker. February 14,

Module 5 Stationary Time Series Models Part 2 AR and ARMA Models and Their Properties Class notes for Statistics 451: Applied Time Series Iowa State University Copyright 2015 W. Q. Meeker. February 14,

ΣΧΕΣΕΙΣ ΑΛΛΗΛΕΞΑΡΤΗΣΗΣ ΚΑΙ ΑΠΟΤΕΛΕΣΜΑΤΙΚΟΤΗΤΑ ΣΤΟ ΧΡΗΜΑΤΙΣΤΗΡΙΟ ΑΞΙΩΝ ΑΘΗΝΩΝ

Ελληνικό Στατιστικό Ινστιτούτο Πρακτικά 20 ου Πανελληνίου Συνεδρίου Στατιστικής (2007), σελ 373-382 ΣΧΕΣΕΙΣ ΑΛΛΗΛΕΞΑΡΤΗΣΗΣ ΚΑΙ ΑΠΟΤΕΛΕΣΜΑΤΙΚΟΤΗΤΑ ΣΤΟ ΧΡΗΜΑΤΙΣΤΗΡΙΟ ΑΞΙΩΝ ΑΘΗΝΩΝ Μαριέττα Σιταρά Τμήμα Επιστήμης

Ελληνικό Στατιστικό Ινστιτούτο Πρακτικά 20 ου Πανελληνίου Συνεδρίου Στατιστικής (2007), σελ 373-382 ΣΧΕΣΕΙΣ ΑΛΛΗΛΕΞΑΡΤΗΣΗΣ ΚΑΙ ΑΠΟΤΕΛΕΣΜΑΤΙΚΟΤΗΤΑ ΣΤΟ ΧΡΗΜΑΤΙΣΤΗΡΙΟ ΑΞΙΩΝ ΑΘΗΝΩΝ Μαριέττα Σιταρά Τμήμα Επιστήμης

1 1 1 2 1 2 2 1 43 123 5 122 3 1 312 1 1 122 1 1 1 1 6 1 7 1 6 1 7 1 3 4 2 312 43 4 3 3 1 1 4 1 1 52 122 54 124 8 1 3 1 1 1 1 1 152 1 1 1 1 1 1 152 1 5 1 152 152 1 1 3 9 1 159 9 13 4 5 1 122 1 4 122 5

1 1 1 2 1 2 2 1 43 123 5 122 3 1 312 1 1 122 1 1 1 1 6 1 7 1 6 1 7 1 3 4 2 312 43 4 3 3 1 1 4 1 1 52 122 54 124 8 1 3 1 1 1 1 1 152 1 1 1 1 1 1 152 1 5 1 152 152 1 1 3 9 1 159 9 13 4 5 1 122 1 4 122 5

Overview. Transition Semantics. Configurations and the transition relation. Executions and computation

Overview Transition Semantics Configurations and the transition relation Executions and computation Inference rules for small-step structural operational semantics for the simple imperative language Transition

Overview Transition Semantics Configurations and the transition relation Executions and computation Inference rules for small-step structural operational semantics for the simple imperative language Transition

6. MAXIMUM LIKELIHOOD ESTIMATION

6 MAXIMUM LIKELIHOOD ESIMAION [1] Maximum Likelihood Estimator (1) Cases in which θ (unknown parameter) is scalar Notational Clarification: From now on, we denote the true value of θ as θ o hen, view θ

6 MAXIMUM LIKELIHOOD ESIMAION [1] Maximum Likelihood Estimator (1) Cases in which θ (unknown parameter) is scalar Notational Clarification: From now on, we denote the true value of θ as θ o hen, view θ

Lecture 21: Properties and robustness of LSE

Lecture 21: Properties and robustness of LSE BLUE: Robustness of LSE against normality We now study properties of l τ β and σ 2 under assumption A2, i.e., without the normality assumption on ε. From Theorem

Lecture 21: Properties and robustness of LSE BLUE: Robustness of LSE against normality We now study properties of l τ β and σ 2 under assumption A2, i.e., without the normality assumption on ε. From Theorem

ΧΩΡΙΚΑ ΟΙΚΟΝΟΜΕΤΡΙΚΑ ΥΠΟΔΕΙΓΜΑΤΑ ΣΤΗΝ ΕΚΤΙΜΗΣΗ ΤΩΝ ΤΙΜΩΝ ΤΩΝ ΑΚΙΝΗΤΩΝ SPATIAL ECONOMETRIC MODELS FOR VALUATION OF THE PROPERTY PRICES

1 ο Συνέδριο Χωρικής Ανάλυσης: Πρακτικά, Αθήνα, 013, Σ. Καλογήρου (Επ.) ISBN: 978-960-86818-6-6 ΧΩΡΙΚΑ ΟΙΚΟΝΟΜΕΤΡΙΚΑ ΥΠΟΔΕΙΓΜΑΤΑ ΣΤΗΝ ΕΚΤΙΜΗΣΗ ΤΩΝ ΤΙΜΩΝ ΤΩΝ ΑΚΙΝΗΤΩΝ Μαριάνθη Στάμου 1*, Άγγελος Μιμής και

1 ο Συνέδριο Χωρικής Ανάλυσης: Πρακτικά, Αθήνα, 013, Σ. Καλογήρου (Επ.) ISBN: 978-960-86818-6-6 ΧΩΡΙΚΑ ΟΙΚΟΝΟΜΕΤΡΙΚΑ ΥΠΟΔΕΙΓΜΑΤΑ ΣΤΗΝ ΕΚΤΙΜΗΣΗ ΤΩΝ ΤΙΜΩΝ ΤΩΝ ΑΚΙΝΗΤΩΝ Μαριάνθη Στάμου 1*, Άγγελος Μιμής και

Lecture 12 Modulation and Sampling

EE 2 spring 2-22 Handou #25 Lecure 2 Modulaion and Sampling The Fourier ransform of he produc of wo signals Modulaion of a signal wih a sinusoid Sampling wih an impulse rain The sampling heorem 2 Convoluion

EE 2 spring 2-22 Handou #25 Lecure 2 Modulaion and Sampling The Fourier ransform of he produc of wo signals Modulaion of a signal wih a sinusoid Sampling wih an impulse rain The sampling heorem 2 Convoluion

Key Formulas From Larson/Farber Elementary Statistics: Picturing the World, Second Edition 2002 Prentice Hall

64_INS.qxd /6/0 :56 AM Page Key Formulas From Larson/Farber Elemenary Saisics: Picuring he World, Second Ediion 00 Prenice Hall CHAPTER Class Widh = round up o nex convenien number Maximum daa enry - Minimum

64_INS.qxd /6/0 :56 AM Page Key Formulas From Larson/Farber Elemenary Saisics: Picuring he World, Second Ediion 00 Prenice Hall CHAPTER Class Widh = round up o nex convenien number Maximum daa enry - Minimum

Econ Spring 2004 Instructor: Prof. Kiefer Solution to Problem set # 5. γ (0)

") Cornell University Department of Economics Econ 60 - Spring 004 Instructor: Prof. Kiefer Solution to Problem set # 5. Autocorrelation function is defined as ρ h = γ h γ 0 where γ h =Cov X t,x t h =E[X

Cornell University Department of Economics Econ 60 - Spring 004 Instructor: Prof. Kiefer Solution to Problem set # 5. Autocorrelation function is defined as ρ h = γ h γ 0 where γ h =Cov X t,x t h =E[X

ΟΙΚΟΝΟΜΕΤΡΙΑ. Βιολέττα Δάλλα. Εθνικό και Καποδιστριακό Πανεπιστήµιο Αθηνών

ΟΙΚΟΝΟΜΕΤΡΙΑ Βιολέττα Δάλλα Τµήµα Οικονοµικών Επιστηµών Εθνικό και Καποδιστριακό Πανεπιστήµιο Αθηνών 1 Εισαγωγή Οικονοµετρία (Econometrics) είναι ο τοµέας της Οικονοµικής επιστήµης που περιγράφει και αναλύει

ΟΙΚΟΝΟΜΕΤΡΙΑ Βιολέττα Δάλλα Τµήµα Οικονοµικών Επιστηµών Εθνικό και Καποδιστριακό Πανεπιστήµιο Αθηνών 1 Εισαγωγή Οικονοµετρία (Econometrics) είναι ο τοµέας της Οικονοµικής επιστήµης που περιγράφει και αναλύει

11. ΠΑΛΙΝΔΡΟΜΗΣΗ ΜΕ ΔΕΔΟΜΕΝΑ ΧΡΟΝΟΣΕΙΡΩΝ

11. ΠΑΛΙΝΔΡΟΜΗΣΗ ΜΕ ΔΕΔΟΜΕΝΑ ΧΡΟΝΟΣΕΙΡΩΝ 11.1 Η ΔΟΚΙΜΑΣΙΑ DURBIN-WATSON Όταν στη γραμική παλινδρόμηση τα σφάλματα δεν είναι ανεξάρτητα αλλά συμπεριφέρονται σύμγωνα με το μοντέλο 1 όπου = συντελεστής αυτοσυσχέτισης

11. ΠΑΛΙΝΔΡΟΜΗΣΗ ΜΕ ΔΕΔΟΜΕΝΑ ΧΡΟΝΟΣΕΙΡΩΝ 11.1 Η ΔΟΚΙΜΑΣΙΑ DURBIN-WATSON Όταν στη γραμική παλινδρόμηση τα σφάλματα δεν είναι ανεξάρτητα αλλά συμπεριφέρονται σύμγωνα με το μοντέλο 1 όπου = συντελεστής αυτοσυσχέτισης

SECTION II: PROBABILITY MODELS

SECTION II: PROBABILITY MODELS 1 SECTION II: Aggregate Data. Fraction of births with low birth weight per province. Model A: OLS, using observations 1 260 Heteroskedasticity-robust standard errors, variant

SECTION II: PROBABILITY MODELS 1 SECTION II: Aggregate Data. Fraction of births with low birth weight per province. Model A: OLS, using observations 1 260 Heteroskedasticity-robust standard errors, variant

Durbin-Levinson recursive method

Durbin-Levinson recursive method A recursive method for computing ϕ n is useful because it avoids inverting large matrices; when new data are acquired, one can update predictions, instead of starting again

Durbin-Levinson recursive method A recursive method for computing ϕ n is useful because it avoids inverting large matrices; when new data are acquired, one can update predictions, instead of starting again

, 1. Παράδειγμα: 1) Όχι σύγχρονη εξωγένεια: Cov y, u Cov y, u 0. 2) Έλλειψη Δυναμικής Πληρότητας: ~ AR(2)

Όχι σύγχρονη εξωγένεια: Cov y, u Cov y, u 0. 2) Έλλειψη Δυναμικής Πληρότητας: ~ AR(2)") αυτοσυσχέτιση Παράδειγμα: e ) Όχι σύγχρονη εξωγένεια: Cov Cov 2) Έλλειψη Δυναμικής Πληρότητας: 2 e 2 (προφανώς αφού έχουμε δείξει ότι Δ.Π. Υ5 ) ~ AR(2) 2 Έλεγχος για αυτοσυσχέτιση με τη στατιστική (Ασυμπτωτικός)...

αυτοσυσχέτιση Παράδειγμα: e ) Όχι σύγχρονη εξωγένεια: Cov Cov 2) Έλλειψη Δυναμικής Πληρότητας: 2 e 2 (προφανώς αφού έχουμε δείξει ότι Δ.Π. Υ5 ) ~ AR(2) 2 Έλεγχος για αυτοσυσχέτιση με τη στατιστική (Ασυμπτωτικός)...

Answers - Worksheet A ALGEBRA PMT. 1 a = 7 b = 11 c = 1 3. e = 0.1 f = 0.3 g = 2 h = 10 i = 3 j = d = k = 3 1. = 1 or 0.5 l =

C ALGEBRA Answers - Worksheet A a 7 b c d e 0. f 0. g h 0 i j k 6 8 or 0. l or 8 a 7 b 0 c 7 d 6 e f g 6 h 8 8 i 6 j k 6 l a 9 b c d 9 7 e 00 0 f 8 9 a b 7 7 c 6 d 9 e 6 6 f 6 8 g 9 h 0 0 i j 6 7 7 k 9

C ALGEBRA Answers - Worksheet A a 7 b c d e 0. f 0. g h 0 i j k 6 8 or 0. l or 8 a 7 b 0 c 7 d 6 e f g 6 h 8 8 i 6 j k 6 l a 9 b c d 9 7 e 00 0 f 8 9 a b 7 7 c 6 d 9 e 6 6 f 6 8 g 9 h 0 0 i j 6 7 7 k 9

Aquinas College. Edexcel Mathematical formulae and statistics tables DO NOT WRITE ON THIS BOOKLET

Aquinas College Edexcel Mathematical formulae and statistics tables DO NOT WRITE ON THIS BOOKLET Pearson Edexcel Level 3 Advanced Subsidiary and Advanced GCE in Mathematics and Further Mathematics Mathematical

Aquinas College Edexcel Mathematical formulae and statistics tables DO NOT WRITE ON THIS BOOKLET Pearson Edexcel Level 3 Advanced Subsidiary and Advanced GCE in Mathematics and Further Mathematics Mathematical

Προβλέψεις ισοτιμιών στο EViews

Προβλέψεις ισοτιμιών στο EViews Θεωρητικό πλαίσιο προβλέψεων σημείου Σημαντικές επιλογές πλαισίου: Τί θα κάνουμε με την πρόβλεψη; Θα την μοιραστούμε με πολλούς πελάτες, που θα την χρησιμοποιήσουν με διαφορετικό

Προβλέψεις ισοτιμιών στο EViews Θεωρητικό πλαίσιο προβλέψεων σημείου Σημαντικές επιλογές πλαισίου: Τί θα κάνουμε με την πρόβλεψη; Θα την μοιραστούμε με πολλούς πελάτες, που θα την χρησιμοποιήσουν με διαφορετικό

Lecture 7: Overdispersion in Poisson regression

Lecture 7: Overdispersion in Poisson regression Claudia Czado TU München c (Claudia Czado, TU Munich) ZFS/IMS Göttingen 2004 0 Overview Introduction Modeling overdispersion through mixing Score test for

Lecture 7: Overdispersion in Poisson regression Claudia Czado TU München c (Claudia Czado, TU Munich) ZFS/IMS Göttingen 2004 0 Overview Introduction Modeling overdispersion through mixing Score test for

Homework 8 Model Solution Section

MATH 004 Homework Solution Homework 8 Model Solution Section 14.5 14.6. 14.5. Use the Chain Rule to find dz where z cosx + 4y), x 5t 4, y 1 t. dz dx + dy y sinx + 4y)0t + 4) sinx + 4y) 1t ) 0t + 4t ) sinx

MATH 004 Homework Solution Homework 8 Model Solution Section 14.5 14.6. 14.5. Use the Chain Rule to find dz where z cosx + 4y), x 5t 4, y 1 t. dz dx + dy y sinx + 4y)0t + 4) sinx + 4y) 1t ) 0t + 4t ) sinx

ΑΝΑΛΥΣΗ ΚΑΙ ΠΡΟΒΛΕΨΗ ΤΟΥ ΣΥΝΟΛΙΚΟΥ ΑΡΙΘΜΟΥ ΤΩΝ ΓΕΩΡΓΙΚΩΝ ΕΛΚΥΣΤΗΡΩΝ ΤΗΣ ΕΛΛΑΔΑΣ ΜΕ ΣΥΝΑΡΤΗΣΕΙΣ ΧΡΟΝΙΚΗΣ ΤΑΣΗΣ

Ελληνικό Στατιστικό Ινστιτούτο Πρακτικά 8 ου Πανελληνίου Συνεδρίου Στατιστικής (2005) σελ.409-46 ΑΝΑΛΥΣΗ ΚΑΙ ΠΡΟΒΛΕΨΗ ΤΟΥ ΣΥΝΟΛΙΚΟΥ ΑΡΙΘΜΟΥ ΤΩΝ ΓΕΩΡΓΙΚΩΝ ΕΛΚΥΣΤΗΡΩΝ ΤΗΣ ΕΛΛΑΔΑΣ ΜΕ ΣΥΝΑΡΤΗΣΕΙΣ ΧΡΟΝΙΚΗΣ

Ελληνικό Στατιστικό Ινστιτούτο Πρακτικά 8 ου Πανελληνίου Συνεδρίου Στατιστικής (2005) σελ.409-46 ΑΝΑΛΥΣΗ ΚΑΙ ΠΡΟΒΛΕΨΗ ΤΟΥ ΣΥΝΟΛΙΚΟΥ ΑΡΙΘΜΟΥ ΤΩΝ ΓΕΩΡΓΙΚΩΝ ΕΛΚΥΣΤΗΡΩΝ ΤΗΣ ΕΛΛΑΔΑΣ ΜΕ ΣΥΝΑΡΤΗΣΕΙΣ ΧΡΟΝΙΚΗΣ

ΤΟΥΡΙΣΤΙΚΗ ΚΑΙ ΟΙΚΟΝΟΜΙΚΗ ΑΝΑΠΤΥΞΗ: ΜΙΑ ΕΜΠΕΙΡΙΚΗ ΕΡΕΥΝΑ ΓΙΑ ΤΗΝ ΕΛΛΑΔΑ ΜΕ ΤΗΝ ΑΝΑΛΥΣΗ ΤΗΣ ΑΙΤΙΟΤΗΤΑΣ

Ελληνικό Στατιστικό Ινστιτούτο Πρακτικά 1 ου Πανελληνίου Συνεδρίου Στατιστικής (008), σελ 157-164 ΤΟΥΡΙΣΤΙΚΗ ΚΑΙ ΟΙΚΟΝΟΜΙΚΗ ΑΝΑΠΤΥΞΗ: ΜΙΑ ΕΜΠΕΙΡΙΚΗ ΕΡΕΥΝΑ ΓΙΑ ΤΗΝ ΕΛΛΑΔΑ ΜΕ ΤΗΝ ΑΝΑΛΥΣΗ ΤΗΣ ΑΙΤΙΟΤΗΤΑΣ Νίκος

Ελληνικό Στατιστικό Ινστιτούτο Πρακτικά 1 ου Πανελληνίου Συνεδρίου Στατιστικής (008), σελ 157-164 ΤΟΥΡΙΣΤΙΚΗ ΚΑΙ ΟΙΚΟΝΟΜΙΚΗ ΑΝΑΠΤΥΞΗ: ΜΙΑ ΕΜΠΕΙΡΙΚΗ ΕΡΕΥΝΑ ΓΙΑ ΤΗΝ ΕΛΛΑΔΑ ΜΕ ΤΗΝ ΑΝΑΛΥΣΗ ΤΗΣ ΑΙΤΙΟΤΗΤΑΣ Νίκος

Estimation for ARMA Processes with Stable Noise. Matt Calder & Richard A. Davis Colorado State University

Estimation for ARMA Processes with Stable Noise Matt Calder & Richard A. Davis Colorado State University rdavis@stat.colostate.edu 1 ARMA processes with stable noise Review of M-estimation Examples of

Estimation for ARMA Processes with Stable Noise Matt Calder & Richard A. Davis Colorado State University rdavis@stat.colostate.edu 1 ARMA processes with stable noise Review of M-estimation Examples of

Areas and Lengths in Polar Coordinates

Kiryl Tsishchanka Areas and Lengths in Polar Coordinates In this section we develop the formula for the area of a region whose boundary is given by a polar equation. We need to use the formula for the

Kiryl Tsishchanka Areas and Lengths in Polar Coordinates In this section we develop the formula for the area of a region whose boundary is given by a polar equation. We need to use the formula for the

ΕΙΣΑΓΩΓΗ ΣΤΗ ΣΤΑΤΙΣΤΙΚΗ ΑΝΑΛΥΣΗ

ΕΙΣΑΓΩΓΗ ΣΤΗ ΣΤΑΤΙΣΤΙΚΗ ΑΝΑΛΥΣΗ ΕΛΕΝΑ ΦΛΟΚΑ Επίκουρος Καθηγήτρια Τµήµα Φυσικής, Τοµέας Φυσικής Περιβάλλοντος- Μετεωρολογίας ΓΕΝΙΚΟΙ ΟΡΙΣΜΟΙ Πληθυσµός Σύνολο ατόµων ή αντικειµένων στα οποία αναφέρονται

ΕΙΣΑΓΩΓΗ ΣΤΗ ΣΤΑΤΙΣΤΙΚΗ ΑΝΑΛΥΣΗ ΕΛΕΝΑ ΦΛΟΚΑ Επίκουρος Καθηγήτρια Τµήµα Φυσικής, Τοµέας Φυσικής Περιβάλλοντος- Μετεωρολογίας ΓΕΝΙΚΟΙ ΟΡΙΣΜΟΙ Πληθυσµός Σύνολο ατόµων ή αντικειµένων στα οποία αναφέρονται

Σχέσεις, Ιδιότητες, Κλειστότητες

Σχέσεις, Ιδιότητες, Κλειστότητες Ορέστης Τελέλης telelis@unipi.gr Τµήµα Ψηφιακών Συστηµάτων, Πανεπιστήµιο Πειραιώς Ο. Τελέλης Πανεπιστήµιο Πειραιώς Σχέσεις 1 / 26 Εισαγωγή & Ορισµοί ιµελής Σχέση R από

Σχέσεις, Ιδιότητες, Κλειστότητες Ορέστης Τελέλης telelis@unipi.gr Τµήµα Ψηφιακών Συστηµάτων, Πανεπιστήµιο Πειραιώς Ο. Τελέλης Πανεπιστήµιο Πειραιώς Σχέσεις 1 / 26 Εισαγωγή & Ορισµοί ιµελής Σχέση R από

Παράδειγμα 1 Προσαρμόζω το μοντέλο χωρίς quarter

Παράδειγμα 1 Προσαρμόζω το μοντέλο χωρίς quarer Τότε προκύπτουν Summary(b) R R Square Adjused R Square Sd. Error of he Esimae Durbin-Wason 1,978(a),957,955 3,98268,328 a Predicors: (Consan), Money Soch

Παράδειγμα 1 Προσαρμόζω το μοντέλο χωρίς quarer Τότε προκύπτουν Summary(b) R R Square Adjused R Square Sd. Error of he Esimae Durbin-Wason 1,978(a),957,955 3,98268,328 a Predicors: (Consan), Money Soch

ΕΡΓΑΣΙΑ ΜΑΘΗΜΑΤΟΣ: ΘΕΩΡΙΑ ΒΕΛΤΙΣΤΟΥ ΕΛΕΓΧΟΥ ΦΙΛΤΡΟ KALMAN ΜΩΥΣΗΣ ΛΑΖΑΡΟΣ

ΑΡΙΣΤΟΤΕΛΕΙΟ ΠΑΝΕΠΙΣΤΗΜΙΟ ΘΕΣΣΑΛΟΝΙΚΗΣ ΤΜΗΜΑ ΜΑΘΗΜΑΤΙΚΩΝ ΜΕΤΑΠΤΥΧΙΑΚΟ ΠΡΟΓΡΑΜΜΑ ΣΠΟΥΔΩΝ ΘΕΩΡΗΤΙΚΗ ΠΛΗΡΟΦΟΡΙΚΗ ΚΑΙ ΘΕΩΡΙΑ ΣΥΣΤΗΜΑΤΩΝ & ΕΛΕΓΧΟΥ ΕΡΓΑΣΙΑ ΜΑΘΗΜΑΤΟΣ: ΘΕΩΡΙΑ ΒΕΛΤΙΣΤΟΥ ΕΛΕΓΧΟΥ ΦΙΛΤΡΟ KALMAN ΜΩΥΣΗΣ

ΑΡΙΣΤΟΤΕΛΕΙΟ ΠΑΝΕΠΙΣΤΗΜΙΟ ΘΕΣΣΑΛΟΝΙΚΗΣ ΤΜΗΜΑ ΜΑΘΗΜΑΤΙΚΩΝ ΜΕΤΑΠΤΥΧΙΑΚΟ ΠΡΟΓΡΑΜΜΑ ΣΠΟΥΔΩΝ ΘΕΩΡΗΤΙΚΗ ΠΛΗΡΟΦΟΡΙΚΗ ΚΑΙ ΘΕΩΡΙΑ ΣΥΣΤΗΜΑΤΩΝ & ΕΛΕΓΧΟΥ ΕΡΓΑΣΙΑ ΜΑΘΗΜΑΤΟΣ: ΘΕΩΡΙΑ ΒΕΛΤΙΣΤΟΥ ΕΛΕΓΧΟΥ ΦΙΛΤΡΟ KALMAN ΜΩΥΣΗΣ

Formal Semantics. 1 Type Logic

Formal Semantics Principle of Compositionality The meaning of a sentence is determined by the meanings of its parts and the way they are put together. 1 Type Logic Types (a measure on expressions) The

Formal Semantics Principle of Compositionality The meaning of a sentence is determined by the meanings of its parts and the way they are put together. 1 Type Logic Types (a measure on expressions) The

Phys460.nb Solution for the t-dependent Schrodinger s equation How did we find the solution? (not required)

") Phys460.nb 81 ψ n (t) is still the (same) eigenstate of H But for tdependent H. The answer is NO. 5.5.5. Solution for the tdependent Schrodinger s equation If we assume that at time t 0, the electron starts

Phys460.nb 81 ψ n (t) is still the (same) eigenstate of H But for tdependent H. The answer is NO. 5.5.5. Solution for the tdependent Schrodinger s equation If we assume that at time t 0, the electron starts

Homework for 1/27 Due 2/5

Name: ID: Homework for /7 Due /5. [ 8-3] I Example D of Sectio 8.4, the pdf of the populatio distributio is + αx x f(x α) =, α, otherwise ad the method of momets estimate was foud to be ˆα = 3X (where

Name: ID: Homework for /7 Due /5. [ 8-3] I Example D of Sectio 8.4, the pdf of the populatio distributio is + αx x f(x α) =, α, otherwise ad the method of momets estimate was foud to be ˆα = 3X (where

Numerical Analysis FMN011

Numerical Analysis FMN011 Carmen Arévalo Lund University carmen@maths.lth.se Lecture 12 Periodic data A function g has period P if g(x + P ) = g(x) Model: Trigonometric polynomial of order M T M (x) =

Numerical Analysis FMN011 Carmen Arévalo Lund University carmen@maths.lth.se Lecture 12 Periodic data A function g has period P if g(x + P ) = g(x) Model: Trigonometric polynomial of order M T M (x) =

5.4 The Poisson Distribution.

The worst thing you can do about a situation is nothing. Sr. O Shea Jackson 5.4 The Poisson Distribution. Description of the Poisson Distribution Discrete probability distribution. The random variable

The worst thing you can do about a situation is nothing. Sr. O Shea Jackson 5.4 The Poisson Distribution. Description of the Poisson Distribution Discrete probability distribution. The random variable

ΓΡΑΜΜΙΚΗ ΜΟΝΤΕΛΟΠΟΙΗΣΗ ΜΗ-ΚΑΝΟΝΙΚΩΝ ΧΡΟΝΟΣΕΙΡΩΝ ΜΕΣΩ ΜΕΤΑΣΧΗΜΑΤΙΣΜΟΥ ΣΕ ΚΑΝΟΝΙΚΕΣ ΧΡΟΝΟΣΕΙΡΕΣ

Ελληνικό Στατιστικό Ινστιτούτο Πρακτικά 7 ου Πανελληνίου Συνεδρίου Στατιστικής (24), σελ. 243-25 ΓΡΑΜΜΙΚΗ ΜΟΝΤΕΛΟΠΟΙΗΣΗ ΜΗ-ΚΑΝΟΝΙΚΩΝ ΧΡΟΝΟΣΕΙΡΩΝ ΜΕΣΩ ΜΕΤΑΣΧΗΜΑΤΙΣΜΟΥ ΣΕ ΚΑΝΟΝΙΚΕΣ ΧΡΟΝΟΣΕΙΡΕΣ Κουγιουµτζής

Ελληνικό Στατιστικό Ινστιτούτο Πρακτικά 7 ου Πανελληνίου Συνεδρίου Στατιστικής (24), σελ. 243-25 ΓΡΑΜΜΙΚΗ ΜΟΝΤΕΛΟΠΟΙΗΣΗ ΜΗ-ΚΑΝΟΝΙΚΩΝ ΧΡΟΝΟΣΕΙΡΩΝ ΜΕΣΩ ΜΕΤΑΣΧΗΜΑΤΙΣΜΟΥ ΣΕ ΚΑΝΟΝΙΚΕΣ ΧΡΟΝΟΣΕΙΡΕΣ Κουγιουµτζής

Πανεπιστήμιο Θεσσαλίας Πολυτεχνική Σχολή Τμήμα Μηχανικών Χωροταξίας, Πολεοδομίας & Περιφερειακής Ανάπτυξης

Πανεπιστήμιο Θεσσαλίας Πολυτεχνική Σχολή Τμήμα Μηχανικών Χωροταξίας, Πολεοδομίας & Περιφερειακής Ανάπτυξης ΜΑΘΗΜΑ ΕΠΙΛΟΓΗΣ: ΟΙΚΟΝΟΜΕΤΡΙΑ Οι παραβιάσεις των σημαντικότερων υποθέσεων των γραμμικών υποδειγμάτων

Πανεπιστήμιο Θεσσαλίας Πολυτεχνική Σχολή Τμήμα Μηχανικών Χωροταξίας, Πολεοδομίας & Περιφερειακής Ανάπτυξης ΜΑΘΗΜΑ ΕΠΙΛΟΓΗΣ: ΟΙΚΟΝΟΜΕΤΡΙΑ Οι παραβιάσεις των σημαντικότερων υποθέσεων των γραμμικών υποδειγμάτων

Correlation Analysis 개념

Correlation Analysis 개념 Bivariate analysis 측정형두변수간의관계분석 상관관계? 두측정형변수의산점도 : 상호직선적관련성을상관계수 (Correlation Coefficient) 측정. 잠재설명 ( 원인 ) 변수 (X s) 상관관계, 잠재변인과결과변수 (Y) 의상관관계 Pearson 상관계수 측정형변수직선관계정도 cov( X, Y

Correlation Analysis 개념 Bivariate analysis 측정형두변수간의관계분석 상관관계? 두측정형변수의산점도 : 상호직선적관련성을상관계수 (Correlation Coefficient) 측정. 잠재설명 ( 원인 ) 변수 (X s) 상관관계, 잠재변인과결과변수 (Y) 의상관관계 Pearson 상관계수 측정형변수직선관계정도 cov( X, Y

SOLUTIONS TO MATH38181 EXTREME VALUES AND FINANCIAL RISK EXAM

SOLUTIONS TO MATH38181 EXTREME VALUES AND FINANCIAL RISK EXAM Solutions to Question 1 a) The cumulative distribution function of T conditional on N n is Pr (T t N n) Pr (max (X 1,..., X N ) t N n) Pr (max

SOLUTIONS TO MATH38181 EXTREME VALUES AND FINANCIAL RISK EXAM Solutions to Question 1 a) The cumulative distribution function of T conditional on N n is Pr (T t N n) Pr (max (X 1,..., X N ) t N n) Pr (max

Εργαστήριο Ανάπτυξης Εφαρμογών Βάσεων Δεδομένων. Εξάμηνο 7 ο

Εργαστήριο Ανάπτυξης Εφαρμογών Βάσεων Δεδομένων Εξάμηνο 7 ο Procedures and Functions Stored procedures and functions are named blocks of code that enable you to group and organize a series of SQL and PL/SQL

Εργαστήριο Ανάπτυξης Εφαρμογών Βάσεων Δεδομένων Εξάμηνο 7 ο Procedures and Functions Stored procedures and functions are named blocks of code that enable you to group and organize a series of SQL and PL/SQL

Multi-dimensional Central Limit Theorem

Mult-dmensonal Central Lmt heorem Outlne () () () t as () + () + + () () () Consder a sequence of ndependent random proceses t, t, dentcal to some ( t). Assume t 0. Defne the sum process t t t t () t ();

Mult-dmensonal Central Lmt heorem Outlne () () () t as () + () + + () () () Consder a sequence of ndependent random proceses t, t, dentcal to some ( t). Assume t 0. Defne the sum process t t t t () t ();

Multi-dimensional Central Limit Theorem

Mult-dmensonal Central Lmt heorem Outlne () () () t as () + () + + () () () Consder a sequence of ndependent random proceses t, t, dentcal to some ( t). Assume t 0. Defne the sum process t t t t () t tme

Mult-dmensonal Central Lmt heorem Outlne () () () t as () + () + + () () () Consder a sequence of ndependent random proceses t, t, dentcal to some ( t). Assume t 0. Defne the sum process t t t t () t tme

EE512: Error Control Coding

EE512: Error Control Coding Solution for Assignment on Finite Fields February 16, 2007 1. (a) Addition and Multiplication tables for GF (5) and GF (7) are shown in Tables 1 and 2. + 0 1 2 3 4 0 0 1 2 3

EE512: Error Control Coding Solution for Assignment on Finite Fields February 16, 2007 1. (a) Addition and Multiplication tables for GF (5) and GF (7) are shown in Tables 1 and 2. + 0 1 2 3 4 0 0 1 2 3

22 .5 Real consumption.5 Real residential investment.5.5.5 965 975 985 995 25.5 965 975 985 995 25.5 Real house prices.5 Real fixed investment.5.5.5 965 975 985 995 25.5 965 975 985 995 25.3 Inflation

22 .5 Real consumption.5 Real residential investment.5.5.5 965 975 985 995 25.5 965 975 985 995 25.5 Real house prices.5 Real fixed investment.5.5.5 965 975 985 995 25.5 965 975 985 995 25.3 Inflation

Second Order RLC Filters

ECEN 60 Circuits/Electronics Spring 007-0-07 P. Mathys Second Order RLC Filters RLC Lowpass Filter A passive RLC lowpass filter (LPF) circuit is shown in the following schematic. R L C v O (t) Using phasor

ECEN 60 Circuits/Electronics Spring 007-0-07 P. Mathys Second Order RLC Filters RLC Lowpass Filter A passive RLC lowpass filter (LPF) circuit is shown in the following schematic. R L C v O (t) Using phasor

Areas and Lengths in Polar Coordinates

Kiryl Tsishchanka Areas and Lengths in Polar Coordinates In this section we develop the formula for the area of a region whose boundary is given by a polar equation. We need to use the formula for the

Kiryl Tsishchanka Areas and Lengths in Polar Coordinates In this section we develop the formula for the area of a region whose boundary is given by a polar equation. We need to use the formula for the

ΧΡΟΝΟΣΕΙΡΕΣ & ΠΡΟΒΛΕΨΕΙΣ-ΜΕΡΟΣ 7 ΕΛΕΓΧΟΙ. (TEST: Unit Root-Cointegration )

") ΧΡΟΝΟΣΕΙΡΕΣ & ΠΡΟΒΛΕΨΕΙΣ-ΜΕΡΟΣ 7 ΕΛΕΓΧΟΙ (TEST: Unit Root-Cointegration ) ΦΑΙΝΟΜΕΝΙΚΗ ΠΑΛΙΝΔΡΟΜΗΣΗ Η στασιμότητα των δεδομένων (χρονοσειρών) είναι θεωρητική προϋπόθεση για την παλινδρόμηση, δηλ. την εκτίμηση

ΧΡΟΝΟΣΕΙΡΕΣ & ΠΡΟΒΛΕΨΕΙΣ-ΜΕΡΟΣ 7 ΕΛΕΓΧΟΙ (TEST: Unit Root-Cointegration ) ΦΑΙΝΟΜΕΝΙΚΗ ΠΑΛΙΝΔΡΟΜΗΣΗ Η στασιμότητα των δεδομένων (χρονοσειρών) είναι θεωρητική προϋπόθεση για την παλινδρόμηση, δηλ. την εκτίμηση

ΟΙΚΟΝΟΜΕΤΡΙΑ. Βιολέττα Δάλλα. Εθνικό και Καποδιστριακό Πανεπιστήµιο Αθηνών

ΟΙΚΟΝΟΜΕΤΡΙΑ Βιολέττα Δάλλα Τµήµα Οικονοµικών Επιστηµών Εθνικό και Καποδιστριακό Πανεπιστήµιο Αθηνών 1 Αυτοσυσχέτιση Αν τα σφάλµατα δεν συσχετίζονται µεταξύ τους, Corr(u t, u s ) = 0 για κάθε t s, t, s

ΟΙΚΟΝΟΜΕΤΡΙΑ Βιολέττα Δάλλα Τµήµα Οικονοµικών Επιστηµών Εθνικό και Καποδιστριακό Πανεπιστήµιο Αθηνών 1 Αυτοσυσχέτιση Αν τα σφάλµατα δεν συσχετίζονται µεταξύ τους, Corr(u t, u s ) = 0 για κάθε t s, t, s

Modbus basic setup notes for IO-Link AL1xxx Master Block

n Modbus has four tables/registers where data is stored along with their associated addresses. We will be using the holding registers from address 40001 to 49999 that are R/W 16 bit/word. Two tables that

n Modbus has four tables/registers where data is stored along with their associated addresses. We will be using the holding registers from address 40001 to 49999 that are R/W 16 bit/word. Two tables that

Tridiagonal matrices. Gérard MEURANT. October, 2008

Tridiagonal matrices Gérard MEURANT October, 2008 1 Similarity 2 Cholesy factorizations 3 Eigenvalues 4 Inverse Similarity Let α 1 ω 1 β 1 α 2 ω 2 T =......... β 2 α 1 ω 1 β 1 α and β i ω i, i = 1,...,

Tridiagonal matrices Gérard MEURANT October, 2008 1 Similarity 2 Cholesy factorizations 3 Eigenvalues 4 Inverse Similarity Let α 1 ω 1 β 1 α 2 ω 2 T =......... β 2 α 1 ω 1 β 1 α and β i ω i, i = 1,...,

D Alembert s Solution to the Wave Equation

D Alembert s Solution to the Wave Equation MATH 467 Partial Differential Equations J. Robert Buchanan Department of Mathematics Fall 2018 Objectives In this lesson we will learn: a change of variable technique

D Alembert s Solution to the Wave Equation MATH 467 Partial Differential Equations J. Robert Buchanan Department of Mathematics Fall 2018 Objectives In this lesson we will learn: a change of variable technique

90 [, ] p Panel nested error structure) : Lagrange-multiple LM) Honda [3] LM ; King Wu, Baltagi, Chang Li [4] Moulton Randolph ANOVA) F p Panel,, p Z

![90 [, ] p Panel nested error structure) : Lagrange-multiple LM) Honda [3] LM ; King Wu, Baltagi, Chang Li [4] Moulton Randolph ANOVA) F p Panel,, p Z](/thumbs/91/107678282.jpg "90 [, ] p Panel nested error structure) : Lagrange-multiple LM) Honda [3] LM ; King Wu, Baltagi, Chang Li [4] Moulton Randolph ANOVA) F p Panel,, p Z") 00 Chinese Journal of Applied Probability and Statistics Vol6 No Feb 00 Panel, 3,, 0034;,, 38000) 3,, 000) p Panel,, p Panel : Panel,, p,, : O,,, nuisance parameter), Tsui Weerahandi [] Weerahandi [] p

00 Chinese Journal of Applied Probability and Statistics Vol6 No Feb 00 Panel, 3,, 0034;,, 38000) 3,, 000) p Panel,, p Panel : Panel,, p,, : O,,, nuisance parameter), Tsui Weerahandi [] Weerahandi [] p

Elements of Information Theory

Elements of Information Theory Model of Digital Communications System A Logarithmic Measure for Information Mutual Information Units of Information Self-Information News... Example Information Measure

Elements of Information Theory Model of Digital Communications System A Logarithmic Measure for Information Mutual Information Units of Information Self-Information News... Example Information Measure

MATHACHij = γ00 + u0j + rij

Stata output for Hierarchical Linear Models. ***************************************. * Unconditional Random Intercept Model. *************************************** MATHACHij = γ00 + u0j + rij. mixed

Stata output for Hierarchical Linear Models. ***************************************. * Unconditional Random Intercept Model. *************************************** MATHACHij = γ00 + u0j + rij. mixed

Predictability and Model Selection in the Context of ARCH Models

Predicabiliy and Model Selecion in he Conex of ARCH Models Savros Degiannakis and Evdokia Xekalaki Deparmen of Saisics Ahens Universiy of Economics and Business 76 Paission Sree 434 Ahens Greece echnical

Predicabiliy and Model Selecion in he Conex of ARCH Models Savros Degiannakis and Evdokia Xekalaki Deparmen of Saisics Ahens Universiy of Economics and Business 76 Paission Sree 434 Ahens Greece echnical

CHAPTER 12: PERIMETER, AREA, CIRCUMFERENCE, AND 12.1 INTRODUCTION TO GEOMETRIC 12.2 PERIMETER: SQUARES, RECTANGLES,

CHAPTER : PERIMETER, AREA, CIRCUMFERENCE, AND SIGNED FRACTIONS. INTRODUCTION TO GEOMETRIC MEASUREMENTS p. -3. PERIMETER: SQUARES, RECTANGLES, TRIANGLES p. 4-5.3 AREA: SQUARES, RECTANGLES, TRIANGLES p.

CHAPTER : PERIMETER, AREA, CIRCUMFERENCE, AND SIGNED FRACTIONS. INTRODUCTION TO GEOMETRIC MEASUREMENTS p. -3. PERIMETER: SQUARES, RECTANGLES, TRIANGLES p. 4-5.3 AREA: SQUARES, RECTANGLES, TRIANGLES p.

Figure A.2: MPC and MPCP Age Profiles (estimating ρ, ρ = 2, φ = 0.03)..

..") Supplemental Material (not for publication) Persistent vs. Permanent Income Shocks in the Buffer-Stock Model Jeppe Druedahl Thomas H. Jørgensen May, A Additional Figures and Tables Figure A.: Wealth and

Supplemental Material (not for publication) Persistent vs. Permanent Income Shocks in the Buffer-Stock Model Jeppe Druedahl Thomas H. Jørgensen May, A Additional Figures and Tables Figure A.: Wealth and

16. 17. r t te 2t i t 1. 18 19 Find the derivative of the vector function. 19. r t e t cos t i e t sin t j ln t k. 31 33 Evaluate the integral.

SECTION.7 VECTOR FUNCTIONS AND SPACE CURVES.7 VECTOR FUNCTIONS AND SPACE CURVES A Click here for answers. S Click here for soluions. Copyrigh Cengage Learning. All righs reserved.. Find he domain of he

SECTION.7 VECTOR FUNCTIONS AND SPACE CURVES.7 VECTOR FUNCTIONS AND SPACE CURVES A Click here for answers. S Click here for soluions. Copyrigh Cengage Learning. All righs reserved.. Find he domain of he

Asymptotic distribution of MLE

Asymptotic distribution of MLE Theorem Let {X t } be a causal and invertible ARMA(p,q) process satisfying Φ(B)X = Θ(B)Z, {Z t } IID(0, σ 2 ). Let ( ˆφ, ˆϑ) the values that minimize LL n (φ, ϑ) among those

Asymptotic distribution of MLE Theorem Let {X t } be a causal and invertible ARMA(p,q) process satisfying Φ(B)X = Θ(B)Z, {Z t } IID(0, σ 2 ). Let ( ˆφ, ˆϑ) the values that minimize LL n (φ, ϑ) among those

Math221: HW# 1 solutions

Math: HW# solutions Andy Royston October, 5 7.5.7, 3 rd Ed. We have a n = b n = a = fxdx = xdx =, x cos nxdx = x sin nx n sin nxdx n = cos nx n = n n, x sin nxdx = x cos nx n + cos nxdx n cos n = + sin

Math: HW# solutions Andy Royston October, 5 7.5.7, 3 rd Ed. We have a n = b n = a = fxdx = xdx =, x cos nxdx = x sin nx n sin nxdx n = cos nx n = n n, x sin nxdx = x cos nx n + cos nxdx n cos n = + sin

Section 8.3 Trigonometric Equations

99 Section 8. Trigonometric Equations Objective 1: Solve Equations Involving One Trigonometric Function. In this section and the next, we will exple how to solving equations involving trigonometric functions.

99 Section 8. Trigonometric Equations Objective 1: Solve Equations Involving One Trigonometric Function. In this section and the next, we will exple how to solving equations involving trigonometric functions.

ΕΦΑΡΜΟΣΜΕΝΗ ΑΝΑΛΥΣΗ ΠΑΛΙΝΔΡΟΜΗΣΗΣ ΚΑΙ ΔΙΑΣΠΟΡΑΣ (ΝΠΣ) & ΕΦΑΡΜΟΣΜΕΝΗ ΣΤΑΤΙΣΤΙΚΗ (ΠΠΣ) (6o Εξάμηνο Μαθηματικών) Ιανουάριος 2008

& ΕΦΑΡΜΟΣΜΕΝΗ ΣΤΑΤΙΣΤΙΚΗ (ΠΠΣ) (6o Εξάμηνο Μαθηματικών) Ιανουάριος 2008") ΕΦΑΡΜΟΣΜΕΝΗ ΑΝΑΛΥΣΗ ΠΑΛΙΝΔΡΟΜΗΣΗΣ ΚΑΙ ΔΙΑΣΠΟΡΑΣ (ΝΠΣ) & ΕΦΑΡΜΟΣΜΕΝΗ ΣΤΑΤΙΣΤΙΚΗ (ΠΠΣ) (6o Εξάμηνο Μαθηματικών) Ιανουάριος 008 Επώνυμο... Όνομα... A.E.M.... Εξάμηνο... Θέμα Θέμα Θέμα 3 Θέμα 4 Βαθμός ΝΠΣ

ΕΦΑΡΜΟΣΜΕΝΗ ΑΝΑΛΥΣΗ ΠΑΛΙΝΔΡΟΜΗΣΗΣ ΚΑΙ ΔΙΑΣΠΟΡΑΣ (ΝΠΣ) & ΕΦΑΡΜΟΣΜΕΝΗ ΣΤΑΤΙΣΤΙΚΗ (ΠΠΣ) (6o Εξάμηνο Μαθηματικών) Ιανουάριος 008 Επώνυμο... Όνομα... A.E.M.... Εξάμηνο... Θέμα Θέμα Θέμα 3 Θέμα 4 Βαθμός ΝΠΣ

ΣΧΟΛΗ ΔΙΟΙΚΗΣΗΣ ΕΠΙΧΕΙΡΗΣΕΩΝ ΤΜΗΜΑ ΟΡΓΑΝΩΣΗΣ ΚΑΙ ΔΙΟΙΚΗΣΗΣ ΕΠΙΧΕΙΡΗΣΕΩΝ ΔΙΔΑΣΚΩΝ: ΘΑΝΑΣΗΣ ΚΑΖΑΝΑΣ. Οικονομετρία

ΣΧΟΛΗ ΔΙΟΙΚΗΣΗΣ ΕΠΙΧΕΙΡΗΣΕΩΝ ΤΜΗΜΑ ΟΡΓΑΝΩΣΗΣ ΚΑΙ ΔΙΟΙΚΗΣΗΣ ΕΠΙΧΕΙΡΗΣΕΩΝ ΔΙΔΑΣΚΩΝ: ΘΑΝΑΣΗΣ ΚΑΖΑΝΑΣ Οικονομετρία 5.1 Αυτοσυσχέτιση: Εισαγωγή Συχνά, η υπόθεση της μη αυτοσυσχέτισης ή σειριακής συσχέτισης

ΣΧΟΛΗ ΔΙΟΙΚΗΣΗΣ ΕΠΙΧΕΙΡΗΣΕΩΝ ΤΜΗΜΑ ΟΡΓΑΝΩΣΗΣ ΚΑΙ ΔΙΟΙΚΗΣΗΣ ΕΠΙΧΕΙΡΗΣΕΩΝ ΔΙΔΑΣΚΩΝ: ΘΑΝΑΣΗΣ ΚΑΖΑΝΑΣ Οικονομετρία 5.1 Αυτοσυσχέτιση: Εισαγωγή Συχνά, η υπόθεση της μη αυτοσυσχέτισης ή σειριακής συσχέτισης

Επιτόκια, Πληθωρισμός και Έλλειμμα (10.2, 12.6, 18.2, 18.6, 18.7)

") Επιτόκια, Πληθωρισμός και Έλλειμμα (10.2, 12.6, 18.2, 18.6, 18.7) 1 Dependent Variable: T_BILLS3 Method: Least Squares Sample: 1948-2003 C 1.25 0.44 2.83 0.01 INFLATION 0.61 0.08 8.09 0.00 DEFICIT 0.70

Επιτόκια, Πληθωρισμός και Έλλειμμα (10.2, 12.6, 18.2, 18.6, 18.7) 1 Dependent Variable: T_BILLS3 Method: Least Squares Sample: 1948-2003 C 1.25 0.44 2.83 0.01 INFLATION 0.61 0.08 8.09 0.00 DEFICIT 0.70

3.4 SUM AND DIFFERENCE FORMULAS. NOTE: cos(α+β) cos α + cos β cos(α-β) cos α -cos β

cos α + cos β cos(α-β) cos α -cos β") 3.4 SUM AND DIFFERENCE FORMULAS Page Theorem cos(αβ cos α cos β -sin α cos(α-β cos α cos β sin α NOTE: cos(αβ cos α cos β cos(α-β cos α -cos β Proof of cos(α-β cos α cos β sin α Let s use a unit circle

3.4 SUM AND DIFFERENCE FORMULAS Page Theorem cos(αβ cos α cos β -sin α cos(α-β cos α cos β sin α NOTE: cos(αβ cos α cos β cos(α-β cos α -cos β Proof of cos(α-β cos α cos β sin α Let s use a unit circle

Solution Series 9. i=1 x i and i=1 x i.

Lecturer: Prof. Dr. Mete SONER Coordinator: Yilin WANG Solution Series 9 Q1. Let α, β >, the p.d.f. of a beta distribution with parameters α and β is { Γ(α+β) Γ(α)Γ(β) f(x α, β) xα 1 (1 x) β 1 for < x

Lecturer: Prof. Dr. Mete SONER Coordinator: Yilin WANG Solution Series 9 Q1. Let α, β >, the p.d.f. of a beta distribution with parameters α and β is { Γ(α+β) Γ(α)Γ(β) f(x α, β) xα 1 (1 x) β 1 for < x

Τουριστική και Οικονοµική Ανάπτυξη: Μια Εµπειρική Ερευνα για την Ελλάδα µε την Ανάλυση της Αιτιότητας

Τουριστική και Οικονοµική Ανάπτυξη: Μια Εµπειρική Ερευνα για την Ελλάδα µε την Ανάλυση της Αιτιότητας Νίκος ριτσάκης Τµήµα Εφαρµοσµένης Πληροφορικής Πανεπιστήµιο Μακεδονίας Περίληψη Η εργασία αυτή εξετάζει

Τουριστική και Οικονοµική Ανάπτυξη: Μια Εµπειρική Ερευνα για την Ελλάδα µε την Ανάλυση της Αιτιότητας Νίκος ριτσάκης Τµήµα Εφαρµοσµένης Πληροφορικής Πανεπιστήµιο Μακεδονίας Περίληψη Η εργασία αυτή εξετάζει

2 Composition. Invertible Mappings

Arkansas Tech University MATH 4033: Elementary Modern Algebra Dr. Marcel B. Finan Composition. Invertible Mappings In this section we discuss two procedures for creating new mappings from old ones, namely,

Arkansas Tech University MATH 4033: Elementary Modern Algebra Dr. Marcel B. Finan Composition. Invertible Mappings In this section we discuss two procedures for creating new mappings from old ones, namely,

& Risk Management , A.T.E.I.

Μεταβλητότητα & Risk Managemen Οικονοµικό Επιµελητήριο της Ελλάδας Επιµορφωτικά Σεµινάρια Σταύρος. Ντεγιαννάκης, Οικονοµικό Πανεπιστήµιο Αθηνών Χρήστος Φλώρος, A.T.E.I. Κρήτης Volailiy - Μεταβλητότητα

Μεταβλητότητα & Risk Managemen Οικονοµικό Επιµελητήριο της Ελλάδας Επιµορφωτικά Σεµινάρια Σταύρος. Ντεγιαννάκης, Οικονοµικό Πανεπιστήµιο Αθηνών Χρήστος Φλώρος, A.T.E.I. Κρήτης Volailiy - Μεταβλητότητα

Probability and Random Processes (Part II)

") Probability and Random Processes (Part II) 1. If the variance σ x of d(n) = x(n) x(n 1) is one-tenth the variance σ x of a stationary zero-mean discrete-time signal x(n), then the normalized autocorrelation

Probability and Random Processes (Part II) 1. If the variance σ x of d(n) = x(n) x(n 1) is one-tenth the variance σ x of a stationary zero-mean discrete-time signal x(n), then the normalized autocorrelation

Μάθημα 2: Mη-στάσιμη χρονοσειρά, έλεγχος μοναδιαίας ρίζας και έλεγχος ανεξαρτησίας

close index close index Μάθημα : Mη-στάσιμη χρονοσειρά, έλεγχος μοναδιαίας ρίζας και έλεγχος ανεξαρτησίας Σταθεροποίηση διασποράς Απαλοιφή τάσης και περιοδικότητας / εποχικότητας Έλεγχοι μοναδιαίας ρίζας

close index close index Μάθημα : Mη-στάσιμη χρονοσειρά, έλεγχος μοναδιαίας ρίζας και έλεγχος ανεξαρτησίας Σταθεροποίηση διασποράς Απαλοιφή τάσης και περιοδικότητας / εποχικότητας Έλεγχοι μοναδιαίας ρίζας

Table 1: Military Service: Models. Model 1 Model 2 Model 3 Model 4 Model 5 Model 6 Model 7 Model 8 Model 9 num unemployed mili mili num unemployed

Tables: Military Service Table 1: Military Service: Models Model 1 Model 2 Model 3 Model 4 Model 5 Model 6 Model 7 Model 8 Model 9 num unemployed mili mili num unemployed mili 0.489-0.014-0.044-0.044-1.469-2.026-2.026

Tables: Military Service Table 1: Military Service: Models Model 1 Model 2 Model 3 Model 4 Model 5 Model 6 Model 7 Model 8 Model 9 num unemployed mili mili num unemployed mili 0.489-0.014-0.044-0.044-1.469-2.026-2.026

Instruction Execution Times

1 C Execution Times InThisAppendix... Introduction DL330 Execution Times DL330P Execution Times DL340 Execution Times C-2 Execution Times Introduction Data Registers This appendix contains several tables

1 C Execution Times InThisAppendix... Introduction DL330 Execution Times DL330P Execution Times DL340 Execution Times C-2 Execution Times Introduction Data Registers This appendix contains several tables

EE 570: Location and Navigation

EE 570: Location and Navigation INS Initialization Aly El-Osery Kevin Wedeward Electrical Engineering Department, New Mexico Tech Socorro, New Mexico, USA In Collaboration with Stephen Bruder Electrical

EE 570: Location and Navigation INS Initialization Aly El-Osery Kevin Wedeward Electrical Engineering Department, New Mexico Tech Socorro, New Mexico, USA In Collaboration with Stephen Bruder Electrical

Potential Dividers. 46 minutes. 46 marks. Page 1 of 11

Potential Dividers 46 minutes 46 marks Page 1 of 11 Q1. In the circuit shown in the figure below, the battery, of negligible internal resistance, has an emf of 30 V. The pd across the lamp is 6.0 V and

Potential Dividers 46 minutes 46 marks Page 1 of 11 Q1. In the circuit shown in the figure below, the battery, of negligible internal resistance, has an emf of 30 V. The pd across the lamp is 6.0 V and

LAD Estimation for Time Series Models With Finite and Infinite Variance

LAD Estimatio for Time Series Moels With Fiite a Ifiite Variace Richar A. Davis Colorao State Uiversity William Dusmuir Uiversity of New South Wales 1 LAD Estimatio for ARMA Moels fiite variace ifiite

LAD Estimatio for Time Series Moels With Fiite a Ifiite Variace Richar A. Davis Colorao State Uiversity William Dusmuir Uiversity of New South Wales 1 LAD Estimatio for ARMA Moels fiite variace ifiite

Queensland University of Technology Transport Data Analysis and Modeling Methodologies

Queensland University of Technology Transport Data Analysis and Modeling Methodologies Lab Session #7 Example 5.2 (with 3SLS Extensions) Seemingly Unrelated Regression Estimation and 3SLS A survey of 206

Queensland University of Technology Transport Data Analysis and Modeling Methodologies Lab Session #7 Example 5.2 (with 3SLS Extensions) Seemingly Unrelated Regression Estimation and 3SLS A survey of 206